🎓MaxDividends Academy Case Study: W.W. Grainger (GWW)

A step-by-step company analysis that teaches you how to apply the MaxDividends strategy in real life.

MaxDividends Mission: Helping people build growing passive income, retire early, and live off dividends.

This series is part of the MaxDividends Academy — where we teach our proven secret Five-Pillar Formula in practice. Each lesson breaks down a real company, showing how to spot lasting dividend payers and avoid traps, step by step.

⭐️ Premium Hub | 🎬 MaxDividends App: 2-Minute Video

Learn Dividend Investing One Stock at a Time

🎓 MaxDividends Academy Case Study: W.W. Grainger (GWW)

Hey — Max here 💪

Before we dive in, let me say a few words.

What you’re about to read comes from our Premium section — the highest‑conviction content where we break down, step by step, how to uncover durable dividend compounders, identify potential future Dividend Kings, and build a passive income stream you can rely on.

This is timeless investing wisdom — tested across multiple cycles — distilled into simple, repeatable actions and tools designed to deliver results. Today, you’re getting it.

In future issues, we’ll share exclusive dividend ideas and under‑the‑radar opportunities — businesses with the operational DNA to become tomorrow’s icons and long‑term dividend growers.

The best part? You’ll see them early. That’s the edge: spotting quality before the crowd, and — with the right process — positioning yourself ahead of the herd rather than chasing performance after it shows up on everyone’s radar.

When you think of industrial supply and the backbone of American maintenance, repair, and operations (MRO), W.W. Grainger is one of the clearest leaders — a scaled distributor with a vast catalog, powerful logistics, and a growing digital engine that keeps factories, warehouses, and facilities running.

It’s also a dividend standout, backed by a long history of consistent dividend increases, disciplined capital allocation, and a shareholder‑friendly approach that blends dividend growth with opportunistic buybacks — supported by resilient demand for “must‑have” supplies rather than “nice‑to‑have” purchases.

The real question is not whether Grainger is a great business.

The question is:

Does GWW fit your plan right now — or is it one to watch and wait for?

In this Deep Dive, GWW goes through the MaxDividends Five‑Pillar Formula — the same straightforward checklist we use to identify companies that can keep paying (and growing) dividends through recessions, rate cycles, and shifting economic conditions.

👉 Let’s break it down step by step.

How This Company Makes Money?

Do I clearly understand how W.W. Grainger earns its money — and does the business make sense?

Grainger makes money in a straightforward, repeatable way: it distributes maintenance, repair, and operations (MRO) products to businesses and institutions, earning a margin between what it sources and what customers pay — layered with value‑added services, fast fulfillment, and a growing digital ordering engine. The core engines:

1️⃣ High‑Touch Solutions (Large Customers)

Grainger serves large enterprises through dedicated sales coverage, inventory programs, and procurement integration. These customers value reliability, technical support, and supply‑chain continuity — and Grainger earns revenue by providing a broad assortment, contracted pricing, and service that reduces downtime and complexity for the buyer.

2️⃣ Endless Assortment (Online)

A major growth driver is Grainger’s online‑led, high‑velocity model — including its “endless assortment” offering that expands SKU breadth and captures smaller orders efficiently. Digital scale, search‑driven demand, and streamlined fulfillment support attractive unit economics and repeat purchasing behavior.

3️⃣ Distribution, Logistics & Service Value

Grainger’s network of distribution centers, branch footprint, and delivery capabilities are not just “costs” — they’re competitive advantages. Speed, product availability, and dependable fulfillment allow Grainger to win share and protect margins, especially when customers prioritize uptime and safety over shopping for the lowest price.

4️⃣ Adjacent Services & Other Revenue

Beyond product sales, Grainger benefits from services that deepen relationships — things like inventory management programs, procurement tools, safety/compliance support, and other customer‑specific solutions. These are typically smaller than product revenue but help retention and increase wallet share over time.

The key strength is that Grainger sits at the intersection of industrial activity, facility operations, and the non‑discretionary need to keep workplaces running — powered by recurring replenishment demand and a distribution model built for scale.

This isn’t a complex black box — it’s a proven, cash‑generative MRO distribution platform with durable customer needs and improving digital leverage.

👉 And yes — this business model is clear, durable, and makes perfect sense.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience a long‑term dividend strategy needs?

Our approach is simple but powerful: focus on reliable, resilient businesses like W.W. Grainger that can raise their dividends year after year. The longer you hold, the more income flows into your pocket — steadily, predictably, and without you having to do anything. That’s the compounding engine behind our strategy.

The MaxDividends Strategy Checklist – Simple Steps to Pick the Right Stocks

Step 1: Dividend History

Our filter: Companies with 15+ years of consistent dividend growth.

Grainger not only qualifies — it shows the same clean, stair‑step pattern of rising dividends year after year on the 15‑year chart, with the annual payout climbing from roughly $2.5 per share in the early 2010s to about $8.8 per share most recently.

This kind of steady, uninterrupted growth is exactly what long‑term dividend investors want to see: no cuts, no freezes — just consistent upward progress that signals durable cash generation and a disciplined, shareholder‑friendly capital return philosophy.

✅ Step 1 passed — W.W. Grainger (GWW) clearly behaves like a true Dividend Eagle, with a long, consistent track record of dividend raises that reflects a resilient MRO distribution business and management’s commitment to sharing that compounding with investors through different economic environments.

Step 2: The Five-Pillar Secret Formula

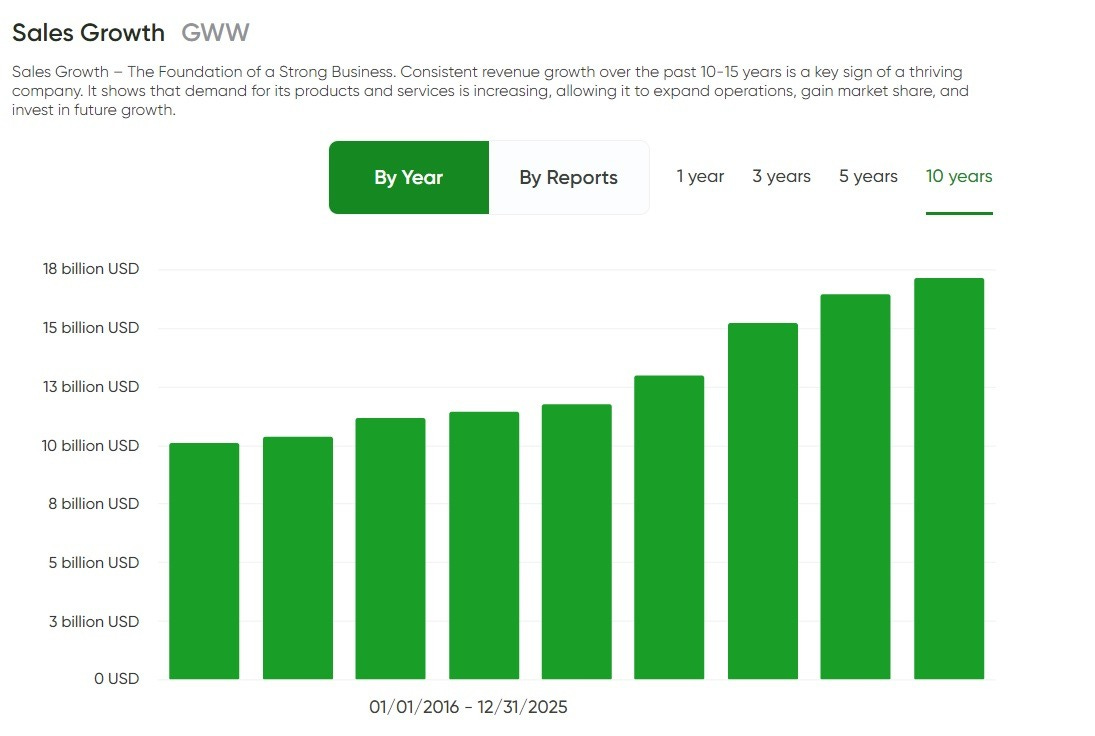

1️⃣ Sales Growth – The Foundation of a Strong Business

Grainger’s revenue story over the last decade looks exactly like what dividend investors prefer: steady progress, not dramatic swings. The chart shows sales rising from around $10B in the mid‑2010s to roughly $17B most recently — a long, upward slope rather than a boom‑and‑bust pattern.

What’s driving it isn’t a one‑off catalyst. Grainger benefits from the unglamorous but essential reality that every plant, warehouse, hospital, and data center needs a constant flow of MRO supplies to avoid downtime. Add in Grainger’s expanding digital capabilities, deeper enterprise relationships, and its ability to deliver quickly from a scaled distribution network — and you get a business that can grow by taking share and increasing customer “stickiness,” even when budgets tighten.

Most importantly, the chart doesn’t show any real “air pockets” in revenue. Sales keep marching higher across the period, which suggests demand is tied to ongoing operations and safety requirements — the kind of spending customers delay last, not first.

✅ Sales Growth Passed — Grainger’s consistent top‑line expansion reflects a resilient, share‑gaining distributor with repeat‑purchase economics, a strong foundation for long‑term dividend growth.

2️⃣ Profit Growth – The Fuel for Dividend Growth

Grainger’s profit trend tells an even stronger story than its revenue line: earnings have expanded while the business scaled, with a noticeable step‑up in the second half of the decade. On the chart, profit rises from roughly $4.0B in the mid‑2010s to about $6.7B most recently.

What matters is why that happened. Grainger isn’t just selling more boxes — it’s getting more efficient at doing it. As the company leaned further into digital ordering, optimized its distribution network, and grew higher‑velocity channels, it improved operating leverage and converted a larger portion of sales into profit. The result is a business that can grow without needing a proportional increase in overhead.

You can also see that profitability doesn’t behave like a fragile cyclical. There are small pauses along the way, but the overall direction stays up, and recent years hold close to peak levels. That resilience fits an MRO distributor whose products are tied to keeping facilities running — demand may fluctuate, but it doesn’t disappear.

✅ Profit Growth Passed — Grainger’s expanding profit base strengthens dividend safety, supports continued dividend raises, and leaves room for buybacks and reinvestment while still compounding shareholder returns.

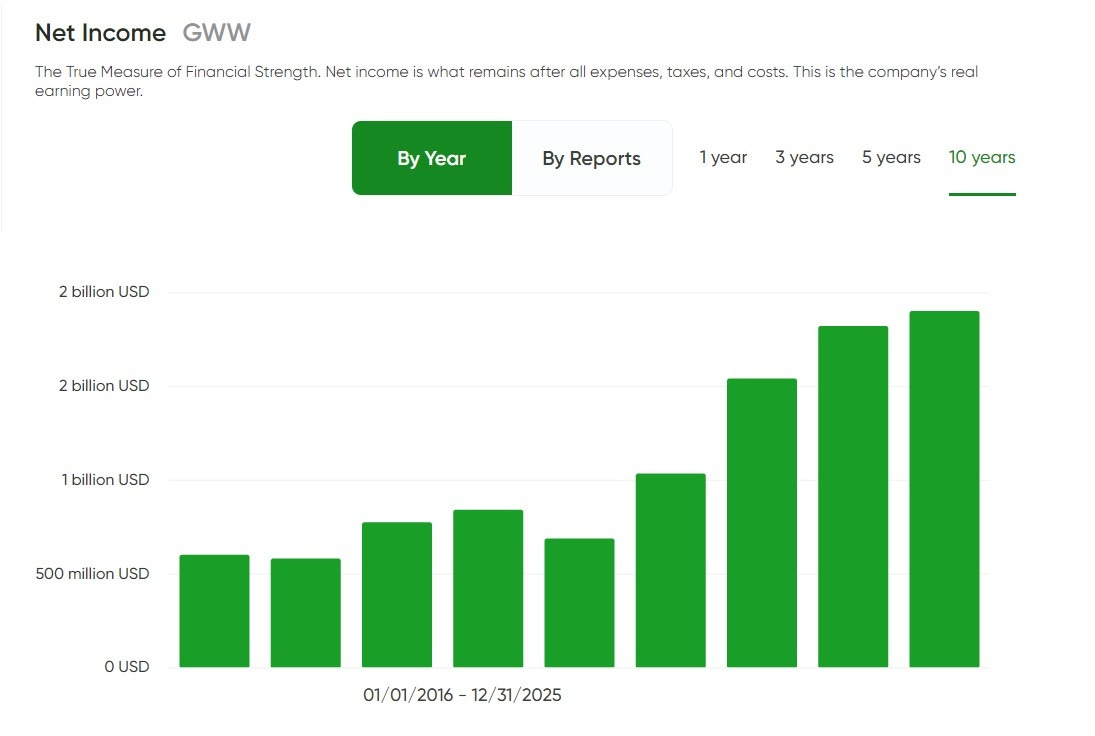

3️⃣ Net Income – True Measure of Strength

Grainger’s net income chart paints the picture dividend investors love: a business that compounds after‑tax earnings over time, not one that lurches around from cycle to cycle. Over the 10‑year window, net income rises from roughly $0.6B in the earlier years to about $1.9B most recently.

Yes, there are a couple of softer years — but the key detail is what happens next: profits re-accelerate and then reset higher, holding near peak levels into the latest period. That pattern suggests Grainger isn’t relying on a temporary boom. It’s improving the underlying economics of the model through scale, better mix, and operating discipline — while serving demand that’s tied to keeping facilities running and compliant.

In other words, even when the macro environment gets noisy, Grainger still converts a meaningful slice of sales into real, bottom‑line earnings — exactly what funds dividend increases, supports buybacks, and keeps the balance sheet flexible.

✅ Net Income Passed — Grainger demonstrates durable, rising earnings power across the decade, reinforcing that its dividend growth is backed by genuine profitability rather than financial engineering.

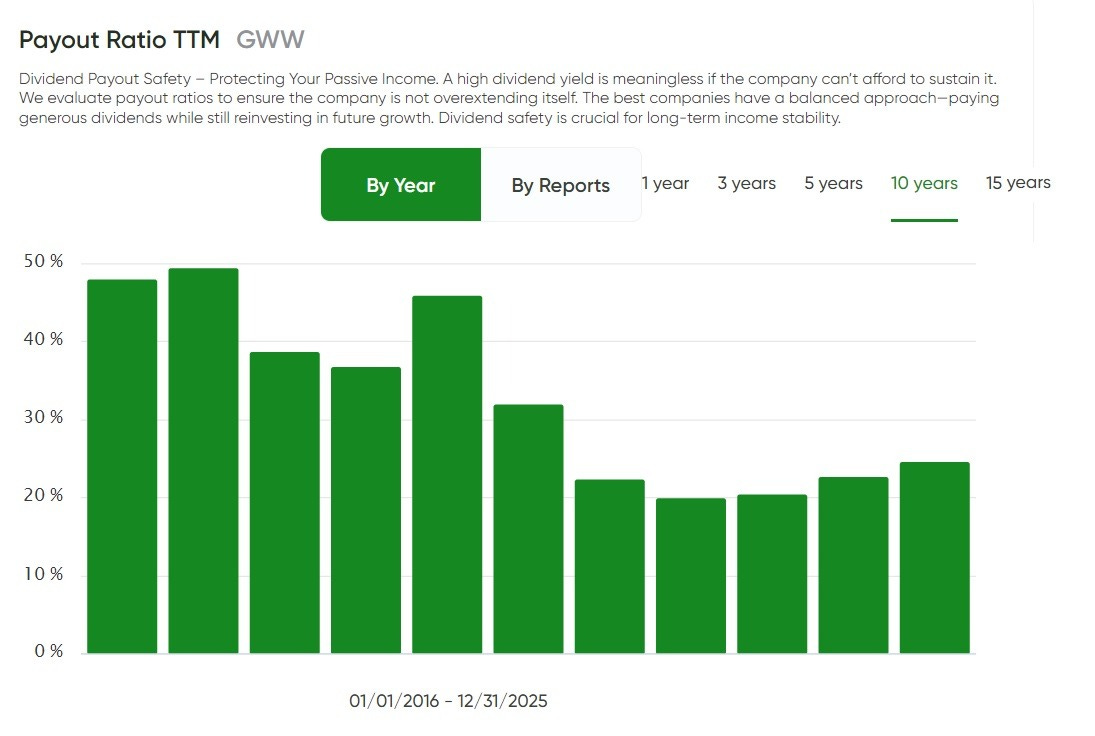

4️⃣ Dividend Payout Safety – Protecting Passive Income

Grainger’s dividend payout ratio looks conservative. On the chart, the payout ratio starts out around the high‑40% range in the earlier part of the decade, then trends materially lower, spending the more recent years roughly in the ~20–25% area.

That tells us two important things. First, the dividend is well covered by earnings, which reduces the risk of a cut if the economy slows or margins temporarily compress. Second, Grainger has plenty of runway to keep raising the dividend even without heroic earnings growth — because it’s not already distributing most of what it makes.

This is the kind of setup long‑term dividend investors want: management can reward shareholders through steady dividend hikes while still retaining ample capital to reinvest in the business (distribution capacity, digital tools, service levels) and to stay flexible with buybacks when valuations are attractive.

✅ Dividend Payout Safety Passed — GWW’s low and improving payout ratio signals a dividend that’s built for durability, with significant room for continued growth without stretching the company’s finances.

5️⃣ Debt Burden – Avoiding Financial Traps

Grainger uses leverage, but the chart shows it’s been kept on a tight leash. Over the last decade, the debt ratio sits in a relatively narrow band — roughly the mid‑0.6s early on — and then drifts lower toward the high‑0.5s in the most recent years. Importantly, it stays well below the kind of levels that would suggest balance‑sheet stress.

That’s a reassuring profile for a distributor. Grainger runs a working‑capital‑heavy model (inventory, fulfillment, logistics), so you want to see debt used as a tool for efficiency, not as a crutch to paper over weak profitability. The downward trend suggests management hasn’t been forced to “borrow its way” through tougher periods — it’s been able to support operations, reinvestment, dividends, and repurchases while gradually strengthening the balance sheet.

In plain terms: even if demand cools, Grainger doesn’t look like it’s carrying a debt load that could crowd out shareholder returns or pressure the dividend policy.

✅ Debt Burden Passed — leverage is moderate and improving, giving GWW the financial flexibility dividend investors want: stability first, optionality second.

Bottom Line: The Company Financial Condition?

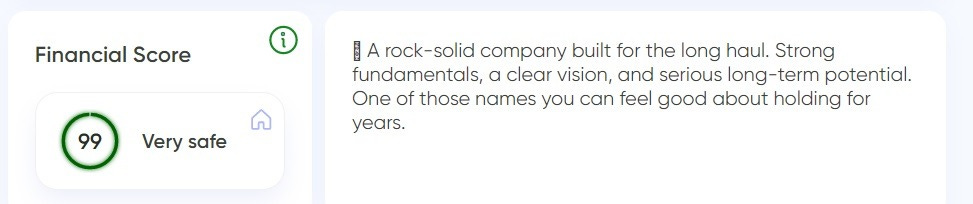

Financial Score 90+ ✅

For W.W. Grainger (GWW), the score comes in at 99 (“Very safe”) — an elite reading. Scores above 90 typically indicate a company with the balance‑sheet strength, earnings consistency, and cash‑generation profile you can feel comfortable owning through multiple market cycles.

MaxDividends Five-Pillar Secret Formula. Step 2 - ✅

By our Five‑Pillar Secret Formula, W.W. Grainger ranks as one of the most dependable dividend growers long‑term income investors can own — steady sales expansion across economic environments, rising profitability, a notably conservative payout ratio with ample room for future hikes, and a debt profile that stays controlled and even improves over time. It clears each quality checkpoint with breathing room.

The Financial Score inside MaxDividends is built on these same five pillars, so you can quickly screen any company — and then validate it with the deeper, step‑by‑step framework behind the score.

✅ Passed: W.W. Grainger (GWW) — Proven Dividend Eagle 🦅

Does It Fit My Plan?

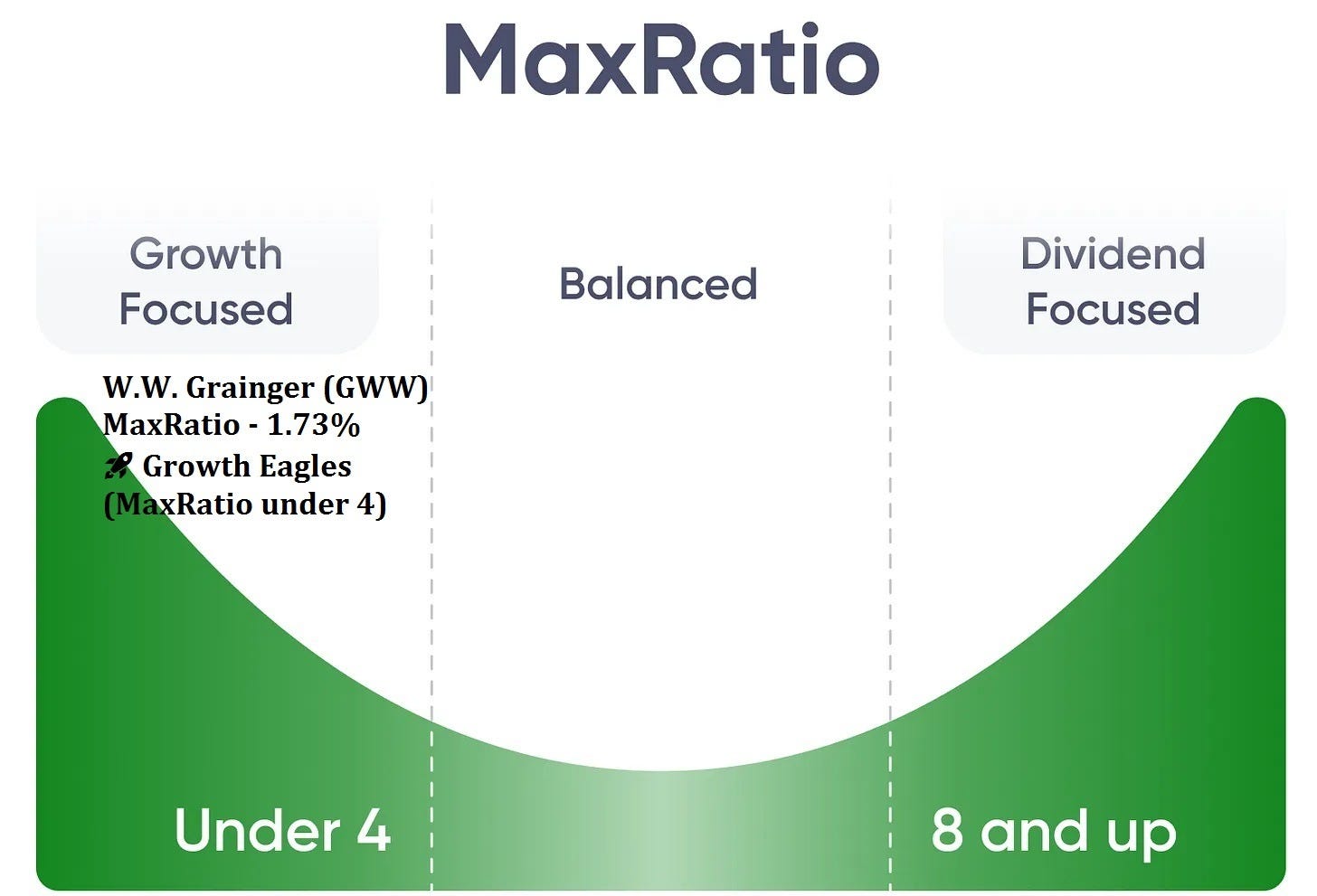

Finding the Right Role for Every Dividend Stock – MaxRatio

Dividend stocks aren’t one-size-fits-all — and that’s precisely what makes them useful when you’re building a portfolio around your priorities. Some companies are best held for long-term price compounding, others deliver a true blend of appreciation and rising income, and a smaller set is primarily about putting meaningful cash in your account today.

That’s the job of MaxRatio. A stock’s dividend profile into three essentials: the yield you get today, how fast the dividend has been growing, and the company’s underlying financial strength.

Taken together, these factors clarify whether a stock belongs in your portfolio as a growth engine, a steady compounder of both capital and income, or a dedicated income workhorse.

🚀 Growth Eagles (MaxRatio under 4) — Capital gains come first. Yields tend to be modest, but they reflect a solid, resilient business, setting you up for substantial long-term wealth while dividends quietly build tomorrow’s income.

⚖️ Balanced Eagles (MaxRatio 4–8) — The best of both worlds. You receive a meaningful payout today, and those checks rise consistently over time, compounding your capital and your cash flows together.

💵 Income Eagles (MaxRatio 8+) — Designed for cash generation. These names offer high current yields with modest, dependable growth, ideal when your priority is straightforward, reliable income.

MaxRatio’s single purpose is to help you assign each dividend stock to the right role, so you can assemble a portfolio that truly reflects your objectives — whether that’s maximum growth, a balance of gains and income, or the highest possible passive cash flow right now.

Let’s Take W.W. Grainger (GWW)

Inside the MaxDividends app, you can open Company Analytics and instantly see the two numbers that matter most for quick dividend positioning: the Financial Score and MaxRatio — no spreadsheets, no manual digging.

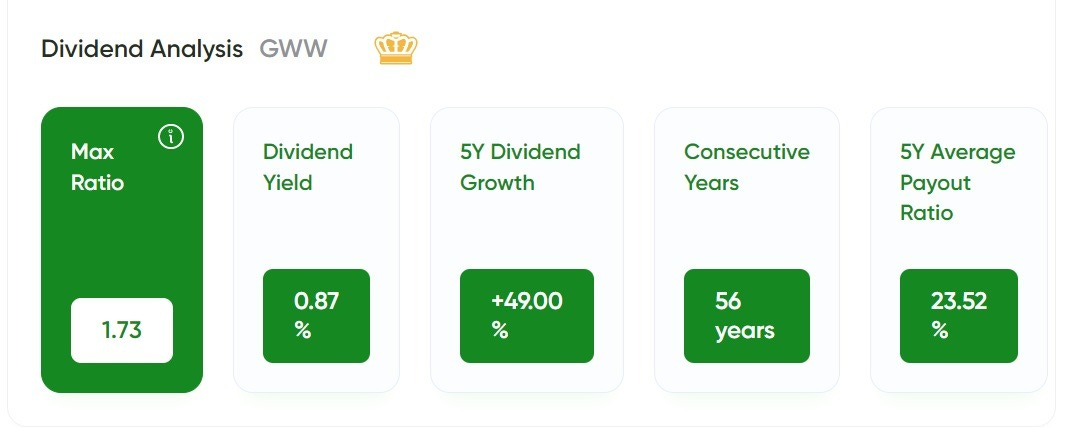

For W.W. Grainger (GWW), the snapshot is clear: MaxRatio 1.73, a 0.87% dividend yield, and a strong +49% cumulative dividend growth over the last 5 years (with 56 consecutive years of dividend raises and a ~23.52% 5‑year average payout ratio).

That combination places Grainger firmly in the 🚀 Growth Eagle bucket. In other words, GWW is designed to compound wealth first, while the dividend grows in the background at an attractive pace. The current yield is intentionally not “high” — but the rapid dividend growth and conservative payout ratio create a long runway for future increases, especially for investors with a multi‑year time horizon.

This profile fits investors who want a high-quality, low-drama compounder — a business you can hold through cycles for capital appreciation, while your dividend checks quietly step higher year after year.

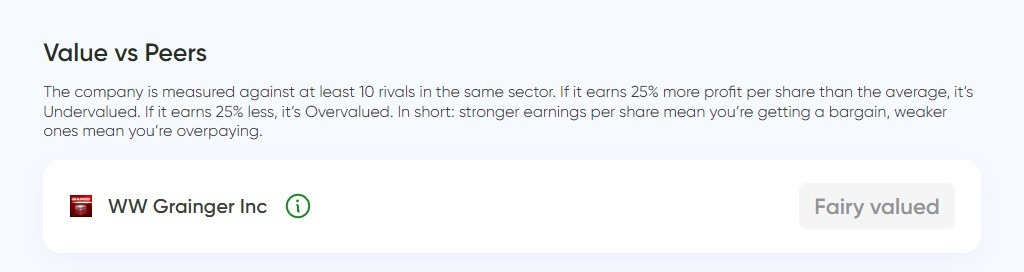

💵 Is the Stock Undervalued Today?

Cheaper than competitors?

✅ According to the MaxDividends App, W.W. Grainger (GWW) currently screens as Fairly Valued versus its peer group.

The market is pricing Grainger close to the industry average — you’re not paying a clear “premium” the way you would with an overvalued name, but you’re also not getting a deep discount relative to comparable industrial/MRO distributors.

In plain English: at today’s price, GWW looks reasonably priced compared with similar companies, suggesting the stock’s quality is largely recognized — and your return will likely depend more on continued execution and dividend growth than on a valuation “re-rating.”

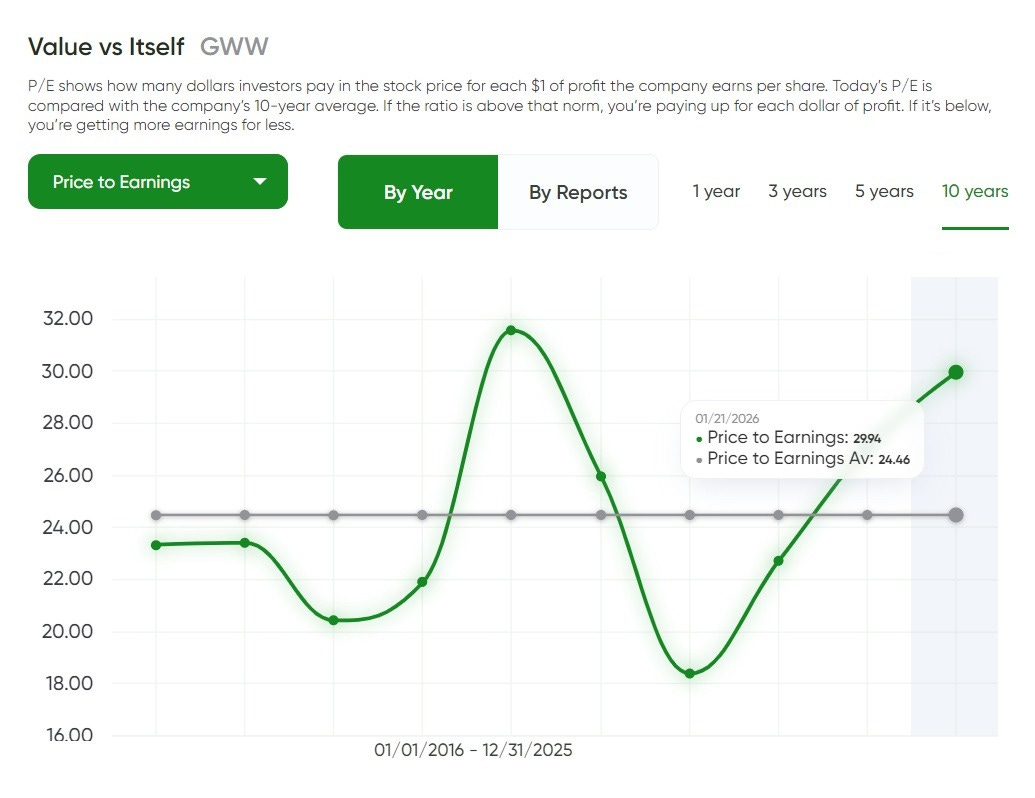

Cheaper than its own history?

⚠️ Expensive vs. its own 10-year average.

Over the last decade, W.W. Grainger (GWW) has typically traded around a ~24.46 average P/E. Today, the chart shows GWW closer to ~29.94, which puts the stock above its long‑term norm.

In plain English: the market is currently assigning Grainger a richer valuation than it usually has per dollar of earnings. That premium can be justified by its execution, resilience, and dividend track record — but based on this metric alone, it doesn’t screen as a “cheap” entry point right now.

Better Yield Than Usual?

⚠️ Yield slightly below its 10-year average.

Right now, Grainger’s dividend yield is about 0.87%, while its long‑term average on the chart sits near 1.45%. That gap tells you the stock is yielding less than it typically has — largely because the share price has appreciated faster than the dividend has grown in the short run.

In plain English: you’re buying GWW with a lower starting yield than normal. That’s not a great fit if your priority is immediate income. But it can make sense for investors who care more about dividend growth + total return, because Grainger’s history of consistent raises means the compounding can still work—just starting from a smaller yield today.

Analyst Consensus

⚠️ Analysts see moderate upside potential for W.W. Grainger as well.

GWW trades around ~$1,047 per share, while the average analyst consensus price target is about ~$1,070 — implying roughly ~2% upside from here.

In plain English: the market already recognizes most of Grainger’s strengths, so the stock isn’t priced like a bargain. Near‑term appreciation potential looks limited to moderate, with the bigger driver likely being ongoing execution and dividend growth rather than a dramatic valuation re‑rating.

Is This One for Me?

Here’s how W.W. Grainger stacks up under the MaxDividends lens:

How This Company Makes Money?

Do I clearly understand how W.W. Grainger earns its money — and does the business make sense to me?

🟢 Yes: mission‑critical MRO distribution at scale. Grainger makes money by supplying businesses and institutions with maintenance, repair, and operations products and earning a margin on those sales. Its edge comes from a massive assortment, strong supplier relationships, and a fulfillment network built for speed and reliability—plus a growing digital ordering engine that drives efficient repeat purchases. The model is easy to grasp, scalable, and anchored in recurring “keep the lights on” demand that customers can’t simply skip without risking downtime and safety issues.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience I want to see?

🟢 Yes: Grainger has a 56‑year streak of consecutive dividend increases, supported by steadily rising sales and profits over the past decade. The dividend has also grown meaningfully in recent years (+49% cumulative growth over the last 5 years), while the payout ratio remains conservative (about ~23.5% on a 5‑year average), giving management ample room to keep raising the dividend through different economic backdrops. This is exactly the kind of durable, shareholder‑oriented consistency long‑term income investors look for.

Is the Stock Undervalued Today? 💵

⚠️ Not really. In the MaxDividends App, GWW screens as Fairly Valued versus peers, but it looks expensive relative to its own history: the current P/E is ~29.94 versus a 10‑year average around ~24.46. The dividend yield also signals a richer price: ~0.87% today compared with a long‑term average near ~1.45%. Taken together, this points to a high‑quality company that’s priced up — more of a premium compounder than an obvious bargain entry right now.

Does It Fit Your Plan?

Not every dividend stock serves the same purpose — and that’s the beauty of building a portfolio with intention.

My strategy is built around stocks that either pay a meaningful dividend upfront and grow it steadily — or begin with a lower yield but raise it fast enough to compound into serious income over time. With a MaxRatio of 1.73, a current yield of ~0.87%, and an exceptional 56 consecutive years of dividend increases, W.W. Grainger (GWW) fits squarely in the Growth Eagle 🚀 category.

This is a stock built primarily to compound capital, while the dividend grows consistently in the background — supported by a conservative payout profile and strong underlying profitability.

It’s a natural fit for investors who prioritize quality and long-term compounding over maximizing income today, and who are comfortable starting with a smaller yield in exchange for a long runway of dividend growth.

For my $12,000-a-month-in-120-months portfolio, I focus first on Dividend Eagles with MaxRatio 10+ — businesses that are truly built around dividends, either through fast payout growth or high current income with steady future growth.

For my kids’ portfolios, I prioritize a different slice of the same universe: Dividend Eagles with a capital-growth focus — companies that reinvest aggressively and compound value over decades.

Final Take

W.W. Grainger has earned serious respect for doing the “boring” work exceptionally well: keeping customers supplied through supply-chain disruptions, inflation shocks, and shifting industrial demand while still compounding earnings and raising the dividend. It’s exactly the type of business we like to study, track, and ultimately own in MaxDividends-style portfolios — a high-quality operator with a long dividend culture and a model built around essential, repeat-purchase demand.

The business itself clears our quality hurdles with room to spare — a Proven Dividend Eagle with 56 consecutive years of dividend hikes, strong profit trends, a very safe financial profile, and a conservative payout policy.

***

The same simple formula I just used for W.W. Grainger works for any stock. No hype, no noise — just clear steps that let you see whether a company truly fits your plan.

And the best part? This isn’t theory. It’s all already built into the MaxDividends app: the Financial Score, the MaxRatio, the Top Dividend Eagles list, and even my own personal shortlist. Everything in one place, ready whenever you are.

MaxDividends is a treasure chest for dividend investors of any size and focus. Whether you’re after growth, balance, or pure income, you’ll find the tools and the community to back you up.

This series of case studies is here to show you just how simple — and powerful — dividend investing can be. One stock at a time, you’ll see the clarity, the confidence, and the peace of mind that comes from building your own growing stream of passive income.

With respect for your well-being,

Max

🎓 MaxDividends Academy Cases

Someone’s sitting in the shade today because someone planted a tree a long time ago. ― Warren Buffett.

Learn the MaxDividends Way

Start Here

🔑 Explore the Premium Hub (exclusive — upgrade to unlock)

Guides & Step-by-Step

Deep Insights

📖 I ❤️ Dividends: Why I Believe Dividend Investing Is the Best Strategy | E-Book

How Effective is the MaxDividends Strategy for Building Growing Passive Income

Help & Support

Got a question about dividends? Ask Max, your AI Dividend Assistant!

Didn’t get the answer you need? Reach out: max@maxdividends.app or team@maxdividends.app — we’ll help you out.