🎓 MaxDividends Academy Case Study: Tractor Supply (TSCO)

A step-by-step company analysis that teaches you how to apply the MaxDividends strategy in real life.

MaxDividends Mission: Helping people build growing passive income, retire early, and live off dividends.

This series is part of the MaxDividends Academy — where we teach our proven secret Five-Pillar Formula in practice. Each lesson breaks down a real company, showing how to spot lasting dividend payers and avoid traps, step by step.

Learn Dividend Investing One Stock at a Time

🎓 MaxDividends Academy Case Study: Tractor Supply (TSCO)

Hey — Max here 💪

Before we dive in, let me say a few words.

What you’re about to see comes from our Premium section — the top-tier content where we break down, step by step, how to spot the best dividend gems out there. How to find the future Dividend Kings… and sleep well at night knowing your income is built on rock-solid foundations.

It’s the kind of timeless investing wisdom that’s been proven over generations — translated into simple, practical actions and tools that actually work. And today, we’re sharing that knowledge with you.

In the next issues, we’ll also explore exclusive dividend ideas and standout companies — names still flying under the radar, but with every chance to become tomorrow’s household brands, the ones paying dividends for the next 50+ years.

And here’s the best part — you’ll be among the first to know them, spot them, and, with the right mindset, invest before the crowd does.

When it comes to quietly reliable businesses that just keep winning, few beat Tractor Supply. It’s not flashy, it’s not tech, but it’s a compounding machine built around small-town America — farmers, ranchers, and homeowners who keep the country running.

This is one of those companies that proves the power of simple, essential business models. Tractor Supply sells products people always need — feed, tools, hardware, and outdoor essentials. Add a loyal customer base, strong margins, and 15+ years of dividend growth, and you’ve got a model of stability in motion.

The question is — does Tractor Supply fit my / your plan right now, or not?

On this example, I’ll show you exactly how I look at Tractor Supply, how it fits (or doesn’t fit) my plan, and how I walk through the steps to reach a fact-based conclusion for myself and my investments. No guessing, no hype — just the MaxDividends framework in action. Step by step, it turns a complex decision into something simple and clear, so you can see how the strategy works in real life.

👉 Let’s put TSCO through the Five-Pillar Formula and see where it stands today.

💡 How This Company Makes Money?

Do I clearly understand how Tractor Supply (TSCO) earns its money — and does the business make sense to me?

Tractor Supply makes money the old-fashioned way — by selling the things rural America needs every single day. From livestock feed to tools, fencing, boots, and pet supplies, it’s the go-to store for farmers, ranchers, and homeowners across the country.

The business runs on three simple but powerful pillars:

1️⃣ Core Retail Stores: Over 2,200 locations in 49 states serving rural and suburban communities. The products are essential — feed, fencing, tools, workwear, and outdoor equipment. These aren’t luxury items; they’re the everyday necessities that keep small farms and homesteads running.

2️⃣ E-Commerce & Omnichannel: Tractor Supply has quietly become a digital success story, with over 25% of sales now touched by online activity. The “Buy Online, Pick Up In Store” model works perfectly for their customer base — practical, efficient, and personal.

3️⃣ Neighbor’s Club Loyalty Program: With 30+ million members, it’s the heart of the brand’s customer retention strategy. Repeat purchases, exclusive offers, and personalized deals keep loyal customers coming back month after month.

The company’s strength lies in recurring demand — animals need feed, tools wear out, and rural life doesn’t pause for recessions. Whether the economy is booming or slowing, TSCO stays relevant because it serves the real, everyday needs of its customers.

That combination — essential products, repeat customers, and nationwide reach — is what makes Tractor Supply a durable, steady cash-flow machine built for the long haul.

👉 And yes — this business makes perfect sense to me.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience I want to see?

Our approach is simple but powerful: stick with reliable, resilient businesses that raise their dividends year after year. The longer you hold, the more income flows into your pocket—steadily, predictably, and without you having to lift a finger. That’s the compounding power behind our strategy.

The MaxDividends Strategy Checklist – Simple Steps to Pick the Right Stocks

Step 1: Dividend History

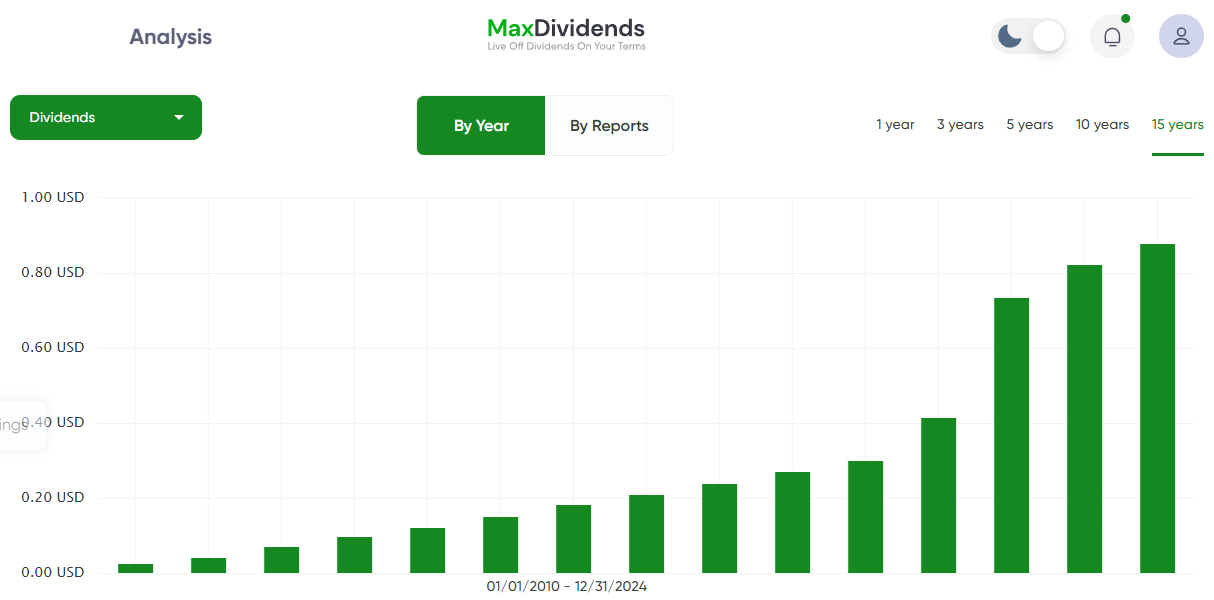

Our filter: Companies with 15+ years of consistent dividend growth.

Tractor Supply checks this box perfectly. The company began paying dividends in 2010 — and as the chart from the MaxDividends App shows, it’s been up and to the right ever since. Every single year brought a raise.

From just a few cents per share in 2010 to nearly $1.00 per quarter by 2024, TSCO’s dividend growth has been relentless. Over that 15-year span, payouts have grown more than 10x, making it one of the strongest performers in the entire retail sector.

The most recent increase came in 2025, when the board approved another ~4.5% raise.

The company’s 5-year dividend growth rate sits around 28% per year, showing not just consistency — but speed. Few retailers in America have managed to deliver both strong earnings expansion and double-digit dividend hikes like this.

✅ Step 1 passed — Tractor Supply is a proven Dividend Eagle 🦅 with a flawless 15-year growth streak, disciplined payout policy, and management fully committed to rewarding long-term shareholders.

Step 2: The Five-Pillar Secret Formula

1️⃣ Sales Growth – The Foundation of a Strong Business

Over the last decade, Tractor Supply has more than doubled its revenue, growing from around $7.8 billion in 2015 to roughly $15.5 billion in 2024 — a clear sign of durable, compounding demand.

The company’s steady climb comes from three growth engines:

Consistent same-store sales gains — people keep coming back for the essentials.

Store expansion — now over 2,200 locations across 49 states, with new stores opening every year.

Digital growth — online orders and “Buy Online, Pick Up In Store” sales now make up over 25% of total revenue.

✅ Sales Growth Passed — demand for everyday rural essentials, loyal customers, and nationwide store expansion keep revenue rising year after year.

2️⃣ Profit Growth – The Fuel for Dividend Growth

Profits at Tractor Supply have expanded right alongside sales, showing the strength and discipline of its operations.

From about $2.1 billion in 2015 to nearly $5.8 billion in 2024, operating profit has more than doubled, powered by steady store growth, strong pricing discipline, and the ability to pass on inflation costs without losing customers.

Margins have remained solid thanks to the company’s focus on private-label brands, efficient logistics, and a loyal base of repeat customers who value reliability over price chasing.

Even during volatile periods — supply chain shocks, cost inflation, or interest rate hikes — Tractor Supply maintained profitability and kept its cash engine running smoothly.

✅ Profit Growth Passed — consistent double-digit earnings expansion driven by scale, pricing power, and loyal repeat customers keeps profits compounding year after year.

3️⃣ Net Income – True Measure of Strength

Tractor Supply’s bottom line tells a story of consistency and discipline. Over the past decade, net income has risen from around $410 million in 2015 to roughly $1.2 billion in 2024, reflecting the company’s ability to grow profitably year after year.

Even through inflation spikes, rising labor costs, and supply chain challenges, TSCO continued to post record earnings — proof of strong customer loyalty and an efficient operating model that holds up in all market conditions.

✅ Net Income Passed — Tractor Supply’s consistent, growing profits highlight a resilient business model and dependable cash generation that dividend investors can count on.

4️⃣ Dividend Payout Safety – Protecting Passive Income

Tractor Supply takes a disciplined approach to dividend payouts, balancing generosity to shareholders with plenty of room to reinvest in growth.

The company’s TTM payout ratio sits around 40%, with a 10-year average close to 30% — a very comfortable level for a mature yet still-expanding retailer.

As shown in the chart from the MaxDividends App, the payout ratio has gradually increased over the years, but always within a safe range. This shows management’s confidence in future cash flow while maintaining a cushion against slowdowns or unexpected costs.

✅ Dividend Payout Safety Passed — balanced and sustainable payout policy, with plenty of room to grow while keeping dividends fully protected by steady, durable cash flows.

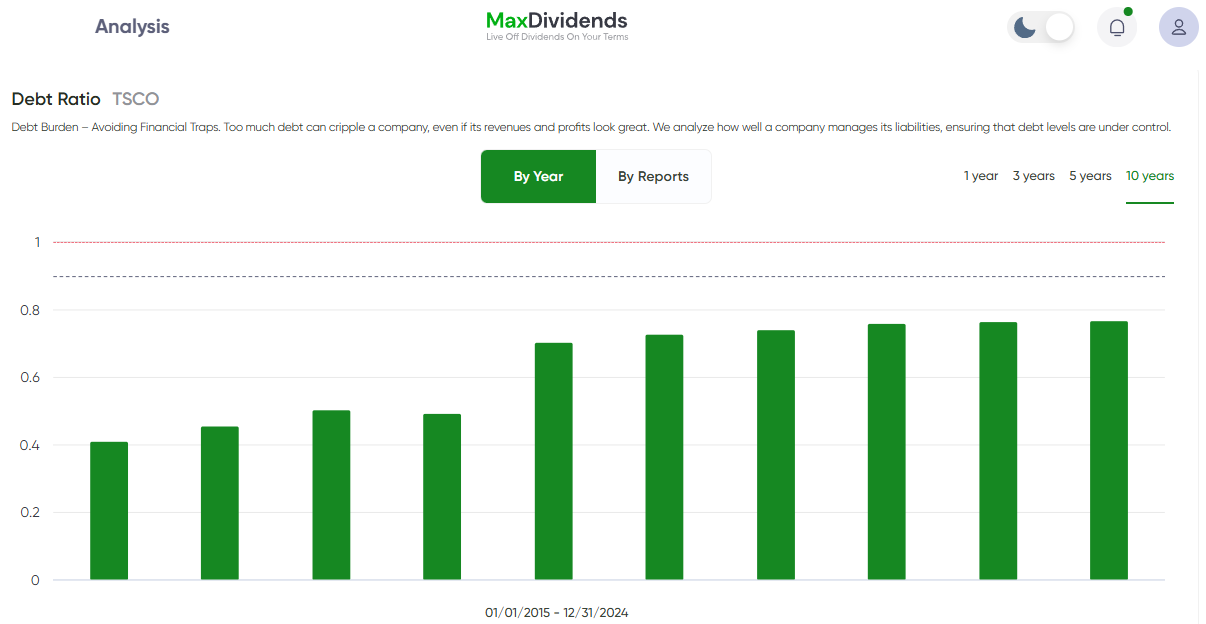

5️⃣ Debt Burden – Avoiding Financial Traps

Tractor Supply maintains a balanced and disciplined approach to debt. Over the last decade, its debt ratio has stayed between 0.4 and 0.8, reflecting a healthy balance between growth financing and financial stability.

While the company has gradually taken on more leverage to support expansion, share buybacks, and capital investments, its cash flow easily covers all obligations, keeping the balance sheet in strong shape.

This is exactly what we like to see: moderate, well-managed debt that supports growth without putting dividends or operations at risk.

✅ Debt Burden Passed — leverage remains controlled, backed by strong free cash flow and prudent capital management. Tractor Supply runs a tight, disciplined balance sheet with no financial red flags.

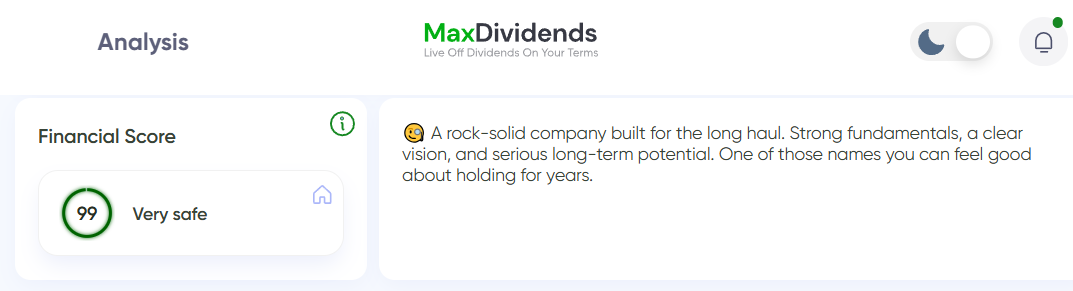

Bottom Line: The Company Financial Condition?

Financial Score 99+ ✅

Think of it as a quick health check for any company. The higher the score, the stronger and safer the business. A score of 90+ means it’s rock-solid and built to last.

MaxDividends Five-Pillar Secret Formula. Step 2 - ✅

By our Five-Pillar Secret Formula, Tractor Supply proves to be one of the most dependable Dividend Eagles in the retail sector — consistent sales growth, rising profits, safe payout ratio, and prudent debt management. It passes every test with confidence.

The Financial Score inside MaxDividends is built on these very same five pillars, giving you a quick, one-glance way to review any company with the full depth of our proven framework behind it.

✅ Passed: Tractor Supply (TSCO) – Proven Dividend Eagle 🦅

Does It Fit My Plan?

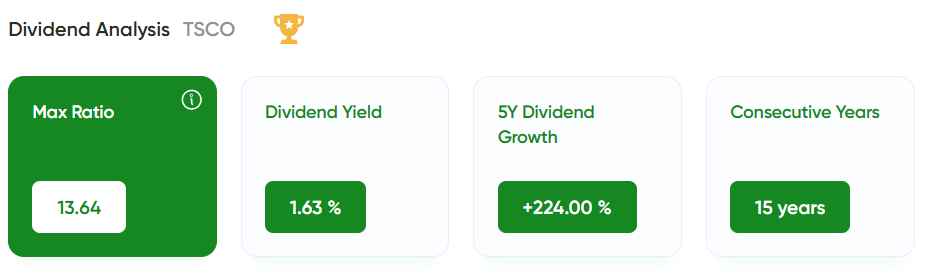

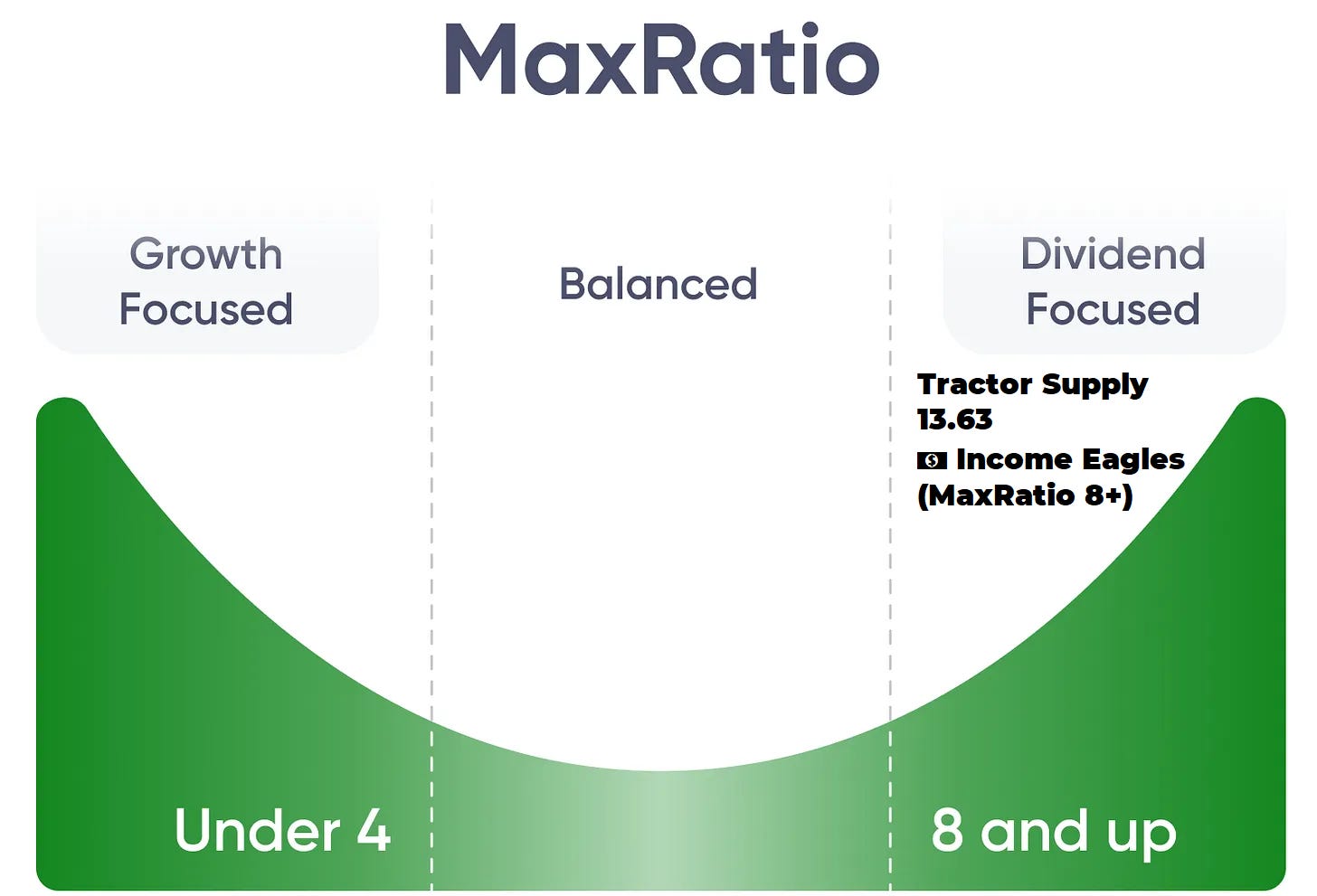

Finding the Right Role for Every Dividend Stock - MaxRatio

Not every dividend stock serves the same purpose — and that’s the beauty of building a portfolio with intention. Some companies are best at growing capital, others strike a balance between growth and income, and a few are built to deliver steady cash right now.

That’s where MaxRatio comes in. It’s a simple metric we created at MaxDividends to help investors cut through the noise and quickly see what a stock is really giving them.

MaxRatio looks at three things: the dividend yield, the pace of dividend growth, and the company’s overall financial strength.

Put together, it shows whether a stock belongs in your portfolio as a growth play, a balanced compounder, or an income leader.

🚀 Growth Eagles (MaxRatio under 4) — Capital growth first. Dividends may be small today, but they’re proof the business is profitable and resilient. These names build wealth over the long haul while quietly compounding income in the background.

⚖️ Balanced Eagles (MaxRatio 4–8) — The best of both worlds. They pay you now and raise those checks steadily year after year, compounding both wealth and income together.

💵 Income Eagles (MaxRatio 8+) — The cash generators. High-yield stocks that put money in your pocket today and usually add a slow but steady growth layer on top. Perfect for reliable, no-drama income.

That’s why MaxRatio matters: it helps you assign the right role to each stock and build a portfolio that works for your goals, whether that’s wealth building, balanced growth, or pure income.

Let’s Take Tractor Supply

In the MaxDividends app, just head to the Company Analytics section. You can quickly check any stock you’re interested in — see the Financial Score and the MaxRatio in one place. It saves a ton of time.

Tractor Supply comes in with a MaxRatio of 13.63, a dividend yield of 1.63%, and a 5-year dividend growth rate of +224%. That combination lands it firmly in the 💵 Income Eagles (MaxRatio 8+) category.

While the yield might look modest, the speed of dividend growth and the company’s rock-solid fundamentals put it among the most shareholder-friendly names in U.S. retail.

In plain terms — TSCO doesn’t just pay; it grows fast. A top-tier dividend grower with the financial strength and consistency to keep rewarding shareholders for years to come.

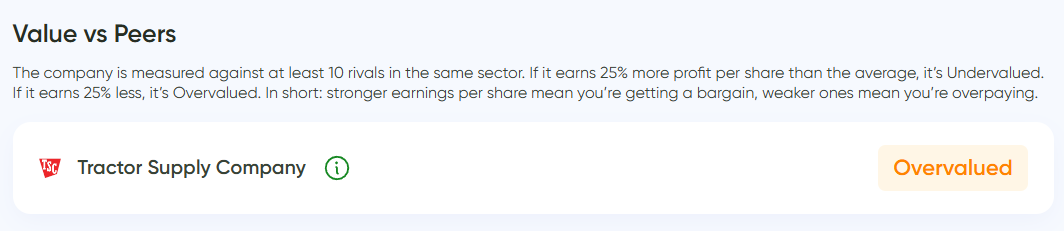

💵 Is the Stock Undervalued Today?

Cheaper than Competitors?

⚠️ According to the MaxDividends App, Tractor Supply (TSCO) currently appears Overvalued compared to its peers. That means investors today are paying a slight premium relative to similar companies in the retail and consumer goods sector.

In plain English: at today’s prices, TSCO trades above the sector average, meaning investors are paying more per dollar of earnings compared to similar companies in the same industry.

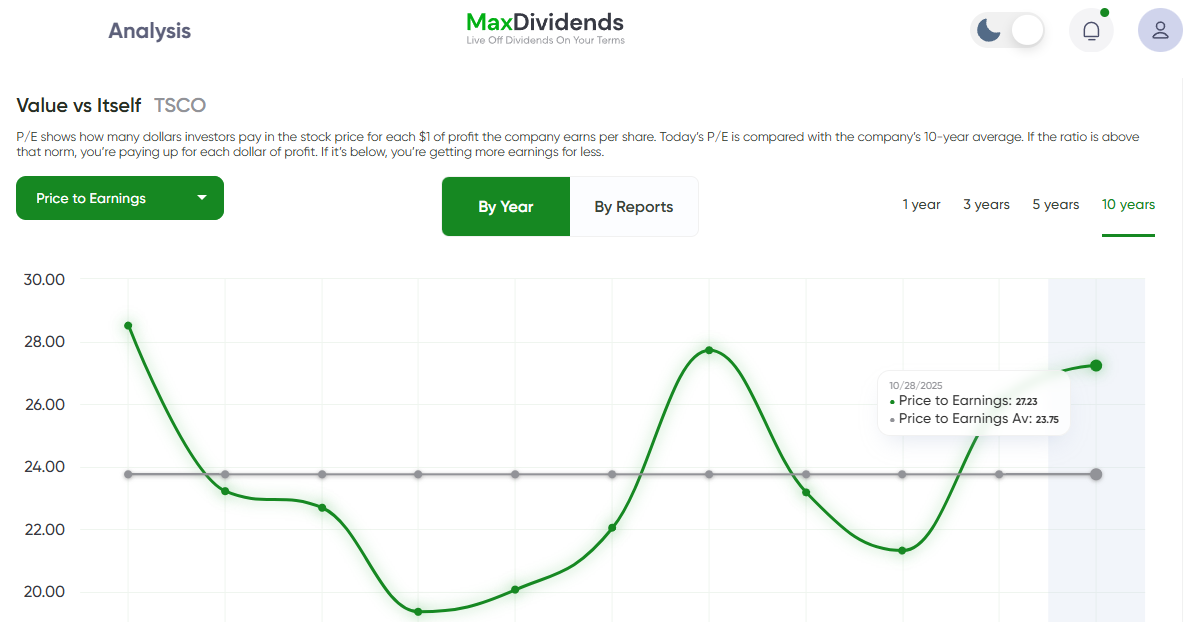

Cheaper than Its Own History?

⚠️ Slightly expensive vs. its own 10-year average.

Over the past decade, Tractor Supply (TSCO) has typically traded at a P/E ratio around 23.8. Today, it stands near 27.2, which means the stock is priced above its long-term average valuation.

In plain English: investors are currently paying more than usual for each dollar of TSCO earnings — a sign the market values the company’s steady growth and consistency, but it’s not a discount level at this point.

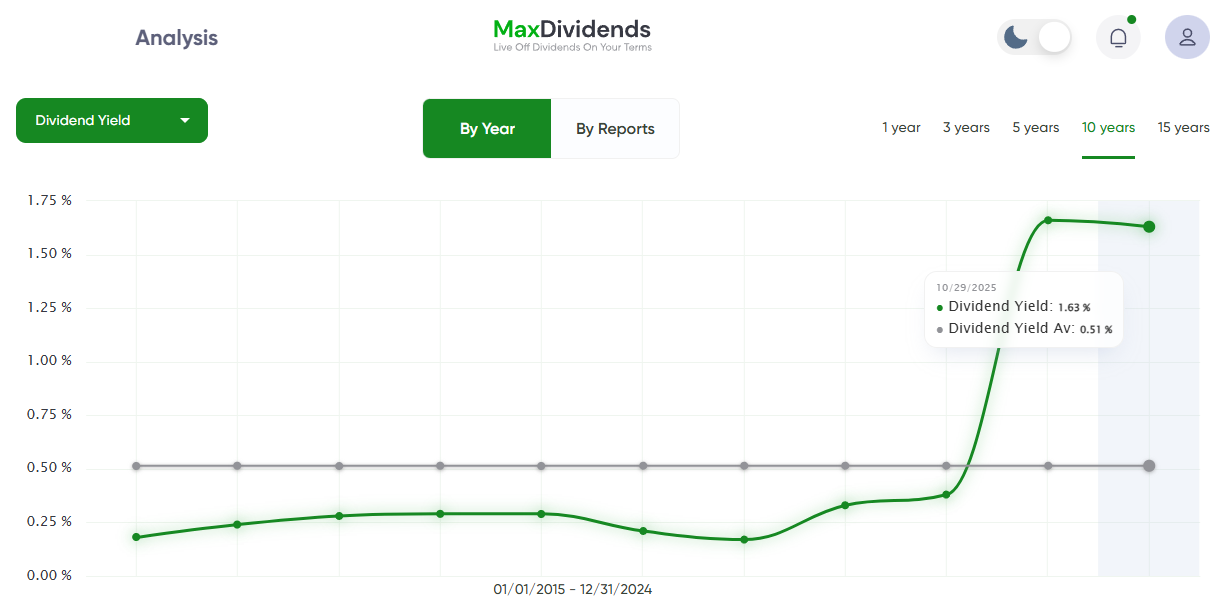

Better Yield Than Usual?

✅ Yield above its 10-year average.

Today, Tractor Supply (TSCO) offers a dividend yield of 1.63%, compared to its 10-year average of 0.51%. That means the current yield is more than three times higher than what investors have typically received over the past decade.

In plain English: investors buying today are locking in a significantly better yield than the long-term average. It’s not high-yield territory, but relative to TSCO’s own history, this is a noticeably more favorable entry point for long-term dividend growth investors.

Analyst Consensus

✅ Analysts see moderate upside potential.

Tractor Supply (TSCO) currently trades around $55.49/share, while the average analyst price target stands near $62 — implying roughly +12% upside from current levels.

In plain English: analysts expect the stock to move higher over time, suggesting that TSCO still has room to grow alongside its steady dividend expansion.

Is This One for Me?

Here’s how the company stacks up under the MaxDividends lens:

How This Company Makes Money?

Do I clearly understand how Microsoft earns its money — and does the business make sense to me?

🟢 Yes: the company sells essential products for rural living — tools, pet supplies, hardware, and farming goods — all supported by steady, recurring demand across the U.S.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience I want to see?

🟢 Yes: 15 straight years of dividend growth, strong profitability, and disciplined financial management with a Financial Score of 99

Is the Stock Undervalued Today? 💵

⚠️ Not quite: according to the MaxDividends App, TSCO is overvalued vs. peers and slightly expensive vs. its own 10-year average, though the current dividend yield (1.63%) is well above its long-term norm (0.51%), offering a slightly better yield entry point than usual.

Does It Fit Your Plan?

Not every dividend stock serves the same purpose — and that’s the beauty of building a portfolio with intention.

My strategy is built around stocks that either pay a solid dividend upfront and grow it steadily — or start with a reasonable yield but raise it at a rocket-like pace. These are the companies that land in the MaxRatio 8+ group.

Final Take

Across all key factors, Tractor Supply meets my personal standards and preferences. It offers a reasonable starting yield, strong dividend growth, and excellent financial strength — exactly the kind of business I like to follow.

I’ve actually owned shares before, buying around $48 per share, and I’d be happy to invest again when the conditions look right.

For now, I’m keeping it on my watchlist, waiting for a more attractive entry point — if the market gives that chance. But make no mistake: this is a company I like, respect, and fully trust to handle a portion of my long-term savings.

***

The same simple formula I just used works for any stock. No hype, no noise — just clear steps that let you see whether a company truly fits your plan.

And the best part? This isn’t theory. It’s all already built into the MaxDividends app: the Financial Score, the MaxRatio, the Top Dividend Eagles list, and even my own personal shortlist. Everything in one place, ready whenever you are.

MaxDividends is a treasure chest for dividend investors of any size and focus. Whether you’re after growth, balance, or pure income, you’ll find the tools and the community to back you up.

This series of case studies is here to show you just how simple — and powerful — dividend investing can be. One stock at a time, you’ll see the clarity, the confidence, and the peace of mind that comes from building your own growing stream of passive income.

With respect for your well-being,

Max

Someone’s sitting in the shade today because someone planted a tree a long time ago. ― Warren Buffett.

Learn the MaxDividends Way

Start Here

🔑 Explore the Premium Hub (exclusive — upgrade to unlock)

Guides & Step-by-Step

Deep Insights

📖 I ❤️ Dividends: Why I Believe Dividend Investing Is the Best Strategy | E-Book

How Effective is the MaxDividends Strategy for Building Growing Passive Income

Help & Support

Got a question about dividends? Ask Max, your AI Dividend Assistant!

Didn’t get the answer you need? Reach out: max@maxdividends.app or team@maxdividends.app — we’ll help you out.