🎓MaxDividends Academy Case Study: Bank OZK (OZK)

A step-by-step company analysis that teaches you how to apply the MaxDividends strategy in real life.

MaxDividends Mission: Helping people build growing passive income, retire early, and live off dividends.

This series is part of the MaxDividends Academy — where we teach our proven secret Five-Pillar Formula in practice. Each lesson breaks down a real company, showing how to spot lasting dividend payers and avoid traps, step by step.

🔓 Request Free Early Access to the MaxDividends App

Learn Dividend Investing One Stock at a Time

🎓 MaxDividends Academy Case Study: Bank OZK (OZK)

Hey — Max here 💪

Before we dive in, a quick reset on what this series really is.

You’re reading an Academy Case — the kind of deep, step-by-step breakdown we normally reserve for our Premium members.

This is where dividend investing becomes practical: how to spot companies that can keep paying (and growing) dividends through ugly markets, how to avoid “high-yield traps,” and how to build an income stream that doesn’t collapse the first time fear hits the market.

No theory. No storytelling. Just classic dividend logic — refined into clear decision rules you can reuse on any stock.

And today, that playbook is open.

In future Academy cases, we’ll keep dissecting stocks that look “obviously good” on the surface — but only reveal their true dividend profile once you inspect the structure underneath.

Because the edge is simple: see the mechanics, not the marketing. Understand what actually funds the dividend — and you stop confusing stability with safety.

Bank OZK is not a consumer staple. It’s not a utility. And it’s not a passive-income bond substitute.

It’s a bank — and banks are balance-sheet machines. Their dividends aren’t powered by product demand or subscription-like revenue. They’re powered by:

credit performance (losses vs recoveries)

deposit stability and funding costs

net interest margin dynamics

capital and regulatory flexibility

OZK can look extremely attractive at first glance:

a long streak of dividend increases

strong profitability for its size

a payout that seems conservative

and often a valuation that screams “cheap”

But when the credit cycle turns, banks don’t behave like classic “sleep-well-at-night” dividend stocks — and that’s where investors get surprised.

That’s exactly why OZK belongs in the Academy. The real question isn’t whether Bank OZK is well-run.

The real question is:

Does OZK fit a dividend strategy built around reliability — or is it a cycle-dependent income play that requires tighter timing, stricter monitoring, and smarter risk control?

In this case study, OZK goes through the MaxDividends Five-Pillar Formula — the same checklist we use to test whether dividends are structurally protected… or simply benefiting from a friendly cycle.

👉 Let’s break it down — step by step.

How This Company Makes Money?

Do I clearly understand how Bank OZK earns its money — and does the business actually make sense?

Bank OZK makes money the “classic bank” way: it gathers funding (mostly deposits) and lends it out, earning the spread between what it earns on assets and what it pays on liabilities — that spread becomes net interest income (NII), the core profit engine. In fact, management pointed directly to record annual net interest income of $1.59B in 2025, helped by loan growth of $2.35B and deposit growth of $2.34B.

This is a balance-sheet business. Not subscriptions. Not consumer products. And that distinction matters: a bank’s income can look stable… until credit costs and funding costs move against it.

Here are the main engines.

1️⃣ Net Interest Income (The Real Revenue Driver)

For OZK, the biggest “why” is simple: NII is the machine.

Key mechanics:

Loan yields (what borrowers pay)

minus deposit + funding costs (what the bank pays depositors)

equals net interest margin / net interest income, which drives earnings power

In Q4 2025, OZK reported net interest income of $407M, and for the full year 2025 it reported net revenues of $1.72B.

Why this matters: if deposit competition heats up (higher rates paid to keep deposits) or if loan yields fall, NII compresses, and earnings soften — even if the bank is “executing well.”

2️⃣ Specialty Lending (Where OZK’s Identity Comes From)

A big part of OZK’s long-term playbook has been specialized lending, particularly through its Real Estate Specialties Group (RESG).

Per the company’s filings, RESG has historically been a meaningful driver of growth and focuses primarily on acquisition, development, and construction (ADC) lending for commercial real estate (CRE).

This can be a high-return lending niche because:

deals can be larger

pricing can be better than vanilla banking

underwriting is often relationship + structure-driven (sponsor quality, collateral, covenants, project economics)

But it also creates a non-negotiable reality for dividend investors: CRE/ADC is cyclical.

When liquidity tightens, cap rates move, refinancing gets harder, or property values reset, credit performance can deteriorate faster than investors expect.

Bank OZK itself markets “large real estate construction projects and lending” as a specialty area — it’s not an incidental exposure.

3️⃣ Diversified Lending Platforms (How OZK Reduces “One-Bucket” Risk)

OZK isn’t only RESG. The bank has been expanding other lending channels to diversify the loan book.

In its filings, OZK describes pursuing growth not just in RESG, but also through Community Banking and other groups such as Indirect Lending, Asset Based Lending, and more — including indirect platforms focused on RV and marine lending.

This matters because:

a “single theme” loan book can create single-theme dividend risk

diversification can smooth results across cycles (in theory)

but the market will still price OZK partly as a CRE-sensitive bank when CRE headlines are loud

So: diversification helps, but it doesn’t magically turn a specialty lender into a consumer staple.

4️⃣ Fees Are Real — But This Isn’t a Fee Business

OZK does generate non-interest income (service charges and other fees), but the scale is typically small relative to spread income.

In Q4 2025, for example, OZK’s non-interest income was $33.6M versus $440.6M in net revenues — useful, but not the core driver.

Translation: this bank is not “asset-management-like.” It does not get paid mostly for services. It gets paid for risk-taking (lending) — and that means the dividend is ultimately funded by credit staying under control.

Why this matters for dividend investors? Bank OZK sits at the intersection of:

interest-rate mechanics (NIM expansion vs compression)

deposit behavior (how expensive it is to keep funding)

credit outcomes (losses arrive in clusters, not evenly)

When credit is calm, a bank dividend can look shockingly safe. When credit turns, the same bank can go from “cheap + safe yield” to “earnings down + provisioning up” very quickly.

And we’ve already seen a reminder of that: in Q4 2025, OZK’s net charge-offs ratio jumped to 1.18% and non-performing loans rose to 1.06% (up from 0.44% a year earlier).

Management argued those charge-offs were tied to a limited number of loans and expects normalization — and importantly, the bank says it had been building reserves ahead of time (American Banker notes ACL grew from about $300M mid-2022 to $632M at year-end 2025).

👉 Yes — the business model makes sense.

👉 But dividend reliability here depends less on “steady consumer demand”… and more on credit + funding conditions across a cycle.

That distinction matters — a lot — in the MaxDividends framework.

Is This a Good Stock to Buy Long Term?

Has Bank OZK shown the kind of consistency and resilience a long‑term dividend strategy needs?

The MaxDividends approach is simple: we don’t chase “one good year.” We build around businesses that raise dividends repeatedly, so your passive income grows in the background while you hold.

That’s the whole point of long-term dividend compounding: the longer you stay invested, the more cash the stock quietly starts sending to you — without you doing anything.

The MaxDividends Strategy Checklist – Simple Steps to Pick the Right Stocks

Step 1: Dividend History

Our filter: Companies with 15+ years of consistent dividend growth.

And this is where Bank OZK immediately gets your attention.

The 15-year dividend chart in the MaxDividends App shows a clean, uninterrupted uptrend. The company increased its annual dividend every single year across the entire period.

Here’s the payout progression (based on the chart landmarks):

2011: less than $0.25 per share

~2015: dividends pushed above $0.50

~2019: dividends moved past $1.00

~2024: a noticeable step-up above $1.50, approaching $2

2025: the tooltip shows $2.18 per share

What stands out most: the strongest acceleration appears in the last three years (2023–2025) — the bars rise faster and the dividend growth becomes more aggressive.

✅ Step 1 passed — Bank OZK shows a clear dividend-growth habit and a long-term commitment to raising shareholder income.

Step 2: The Five-Pillar Secret Formula

1️⃣ Sales Growth – The Foundation of a Strong Business

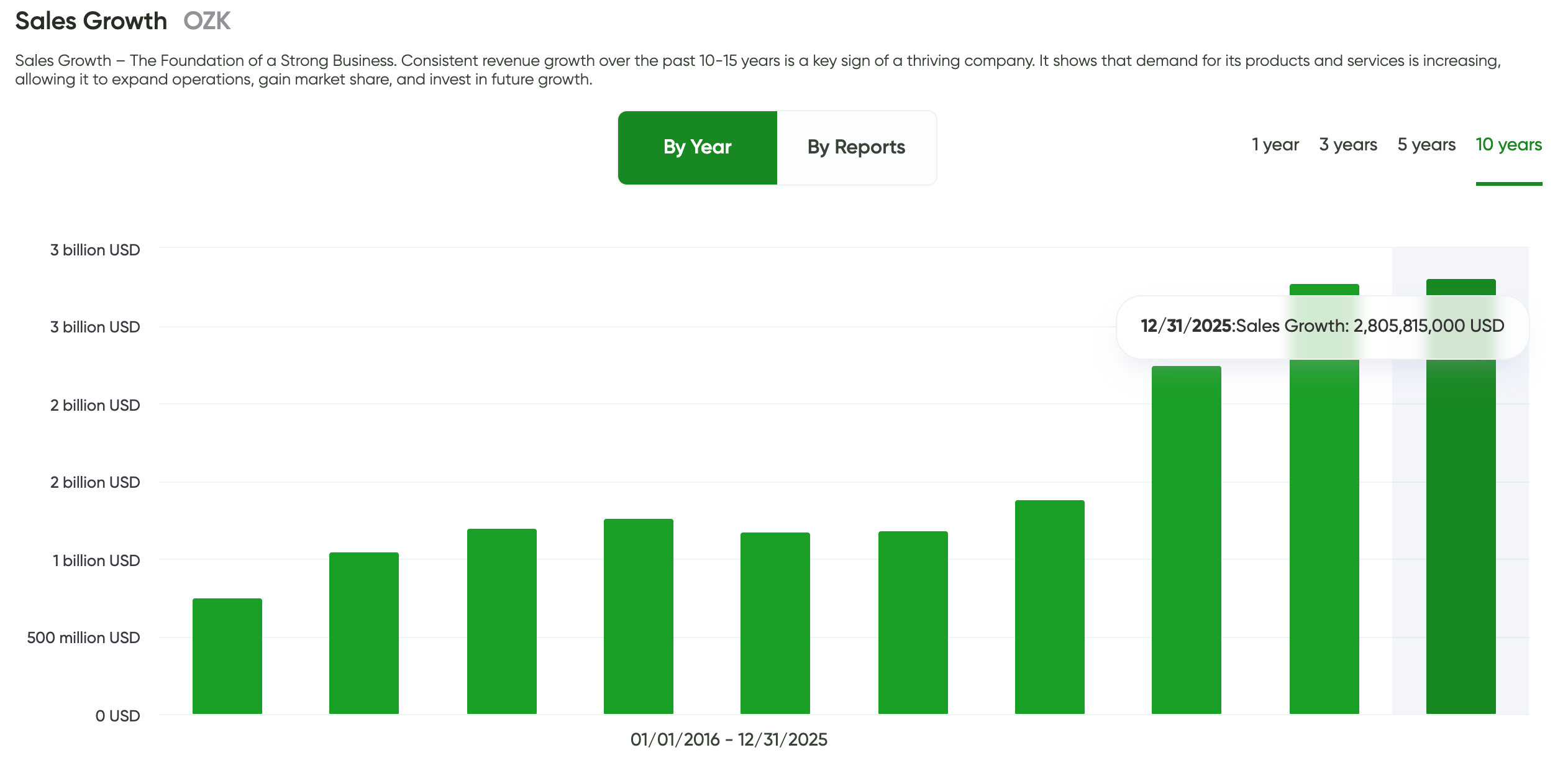

For banks, “sales” isn’t about shopping carts or subscriptions. The cleanest equivalent is total revenue / net revenues — the dollars the bank generates from its lending spread and fees. And on this pillar, Bank OZK looks much stronger than most people assume.

According to the 10-year Sales (Revenue) chart in the MaxDividends App, the long-term trend is clearly upward — not smooth like a consumer staple, but unmistakably expanding.

Here’s the pattern the chart shows:

2016 (start): revenue was below $1B, roughly around $750M

2018–2022: a “steady grind” phase — moderate fluctuations in the $1.2B–$1.4B range

2023 onward: a clear step-change higher

2025 (end): revenue reached a new all-time high, above $2.8B

That last part matters. The jump since 2023 tells you something important about OZK’s operating reality:

the bank has been able to scale earnings power in a higher-rate environment, and/or

expand its balance sheet and net interest income engine, and/or

monetize its lending platform more efficiently than before

Either way, the “sales base” expanded — which is exactly what supports dividends over long holding periods.

✅ Sales Growth passed — Bank OZK shows strong long-term revenue expansion, with a notable acceleration in 2023–2025 that signals a business growing its income engine, not one that’s stagnating.

2️⃣ Profit Growth – The Fuel for Dividend Growth

Dividends don’t grow on “revenue stories.” They grow on profit power.

The Profit Growth chart in the MaxDividends App shows a clear long-term uptrend:

2016: profit just under $750M

2020: a temporary dip back toward the ~$750M level

2021–2025: strong recovery and expansion

2025: profit hit about $1.555B (peak on the chart)

What I like most: profit is scaling alongside sales.

2025 revenue: $2.806B

2025 profit: $1.555B

That’s 55%+ conversion, which signals a highly efficient model.

✅ Profit Growth passed — profits rose meaningfully over the decade, recovered after 2020, and reached a new high in 2025, supporting dividend growth capacity.

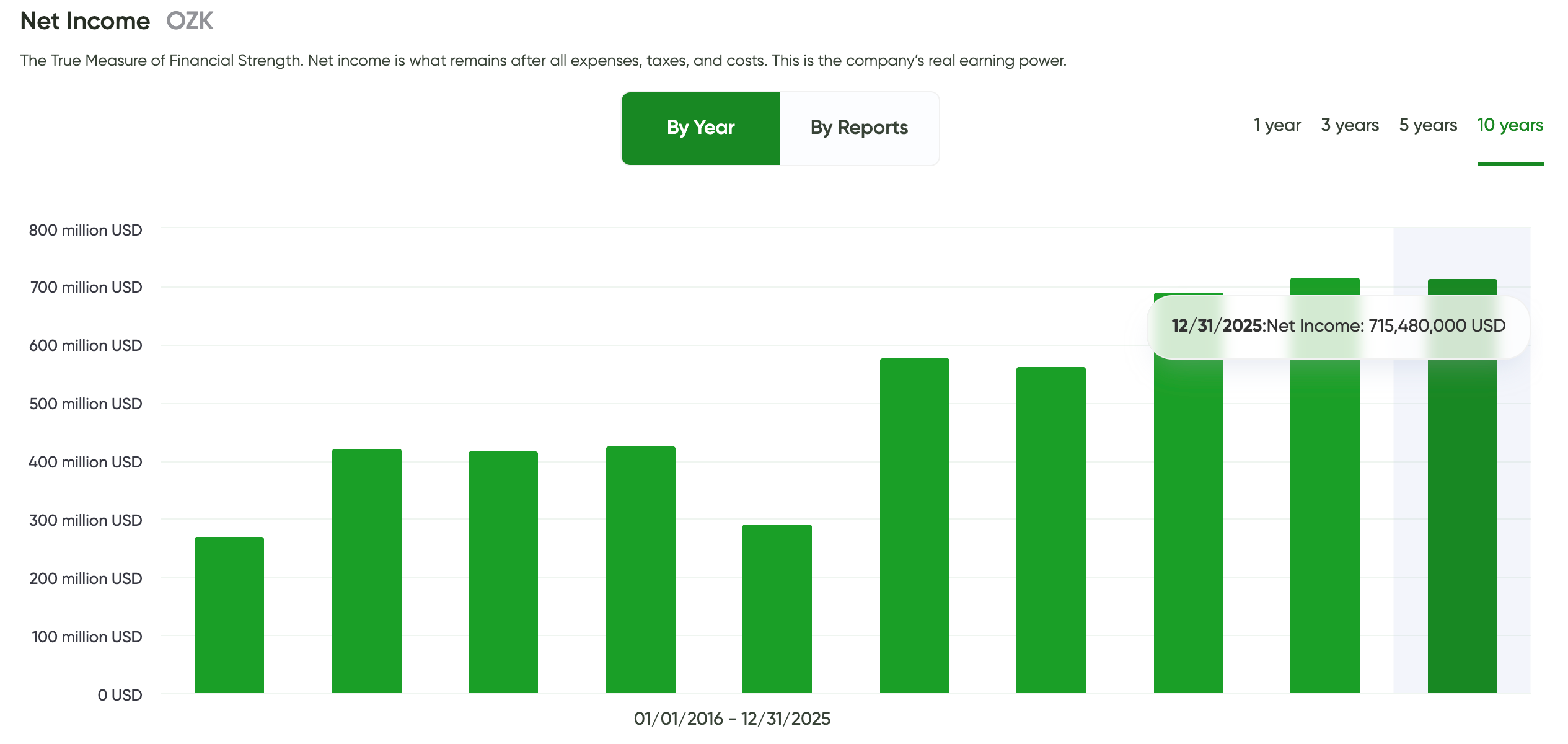

3️⃣ Net Income – True Measure of Strength

For a bank, net income is the clearest “reality check”: after funding costs, credit costs, and operating expenses — what’s left for shareholders?

The Net Income chart in the MaxDividends App shows a business that has grown its earnings power over the decade — with one clear stress dip and then a strong recovery.

2016: about $270M

2020: sharp drop (the low point on the chart), below $300M

2021–2025: steady climb and stabilization

2025: about $715M (and the last ~3 years sit around the $700M+ zone)

OZK’s earnings aren’t perfectly smooth — but the underlying trend is higher, and the bank has demonstrated the ability to rebuild profitability after a weak year.

✅ Net Income passed — long-term earnings power is up materially vs. the mid‑2010s, with a stable $700M+ plateau in recent years.

4️⃣ Dividend Payout Safety – Protecting Passive Income

Here’s the part income investors love: OZK’s dividend isn’t “maxed out.” It’s well inside coverage, which is exactly what gives you durability when the cycle gets choppy.

The 10-year payout ratio history in the MaxDividends App looks conservative overall:

2016–2019: roughly ~21%–28%

2020: a temporary spike to about ~47.5%

2021–2024: back to the ~23%–27% range

2025: about ~33.8%

Latest (02/12/2026): 27.57%

That’s the profile you want: low-to-moderate payout, with room for the dividend to keep growing even if earnings temporarily weaken.

✅ Dividend Payout Safety passed — payout stays conservative across the decade, with the latest level still comfortably covered.

5️⃣ Debt Burden – Avoiding Financial Traps

Banks are different: “debt” is part of the product (deposits and funding). So here we’re looking for stability and no creeping balance-sheet stress, not a “low debt” story like a consumer company.

The Debt Ratio chart in the MaxDividends App is remarkably steady:

Over the last 10 years, it sits roughly in the 0.82–0.85 band

12/31/2025: 0.85

In plain English: the balance-sheet structure looks consistent — no sudden leverage surges, no obvious “we had to gear up to keep the machine running.”

✅ Debt Burden passed — leverage structure is stable across the decade, with no red-flag spikes on the chart.

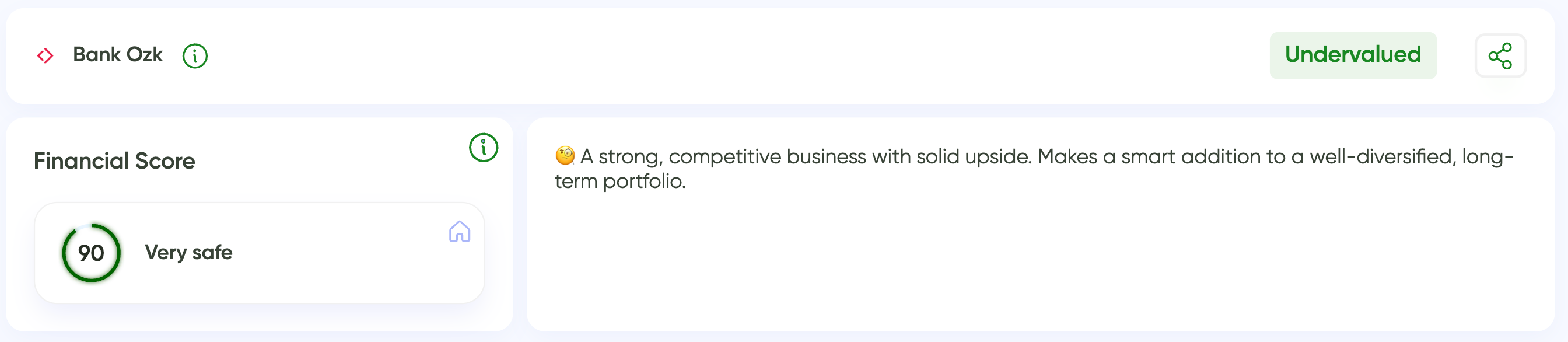

Bottom Line: The Company Financial Condition?

Financial Score: 90 ✅ (Very safe)

Think of this as a fast health check. The higher the Financial Score, the stronger and safer the company looks across the key financial dimensions that matter for dividend investors: growth, profitability, earnings stability, payout discipline, and balance‑sheet risk.

MaxDividends Five-Pillar Secret Formula. Step 2 - ✅

Bank OZK screens as a strong, competitive bank with solid financial resilience and a dividend profile that’s built on real earnings — not financial engineering. And when a company scores “Very safe” and the app flags it as undervalued, that’s typically the exact setup we look for in Academy cases: quality first, price second.

The Financial Score inside MaxDividends combines all five pillars into a single number, giving a clear, at-a-glance view of overall financial safety.

✅ Passed: Bank OZK (OZK) — a financially disciplined dividend grower with strong fundamentals that can fit well inside a diversified long‑term income portfolio.

Does It Fit My Plan?

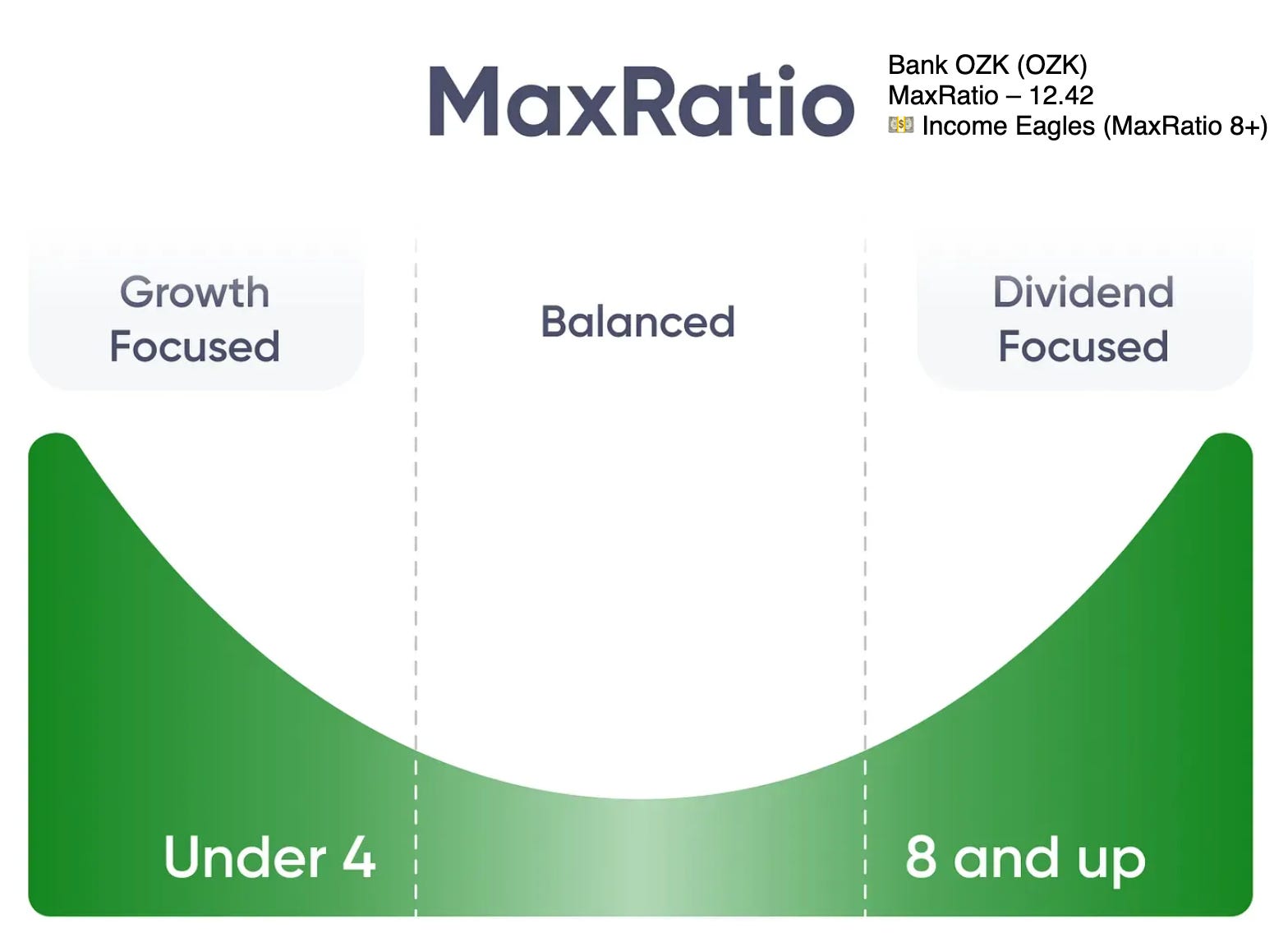

Finding the Right Role for Every Dividend Stock – MaxRatio

Dividend stocks aren’t one-size-fits-all — and that diversity is precisely what enables you to construct a portfolio tailored to your exact needs. Some companies are engineered for aggressive capital expansion, while others deliver a harmonious blend of appreciation and reliable payouts. A select few are optimized exclusively for generating consistent cash flow today.

That’s where MaxRatio comes in. It cuts through the clutter and reveals what each stock actually delivers. The metric weighs three critical factors: the yield you receive today, how aggressively the dividend is expanding, and the underlying financial health of the business.

These three dimensions together tell you whether a stock should function as your growth accelerator, a steady value creator that compounds both gains and income, or your primary cash machine.

🚀 Growth Eagles (MaxRatio below 4) — These prioritize appreciation. Current yields may look modest, but they signal a healthy, durable business. You’re building serious long-term wealth while your dividend quietly compounds into tomorrow’s income stream.

⚖️ Balanced Eagles (MaxRatio 4–8) — The middle path. You earn meaningful dividends right now while watching those payments climb steadily, creating compounding on both your capital and your cash receipts.

💵 Income Eagles (MaxRatio 8+) — Pure income generators. These deliver fat yields today while adding steady, predictable growth — the perfect choice if your priority is hassle-free, dependable cash production.

MaxRatio exists for one reason: it lets you place each dividend holding into its proper role and assemble a portfolio that mirrors your personal objectives — whether you’re chasing explosive growth, seeking balanced gains plus regular payments, or maximizing today’s passive income stream.

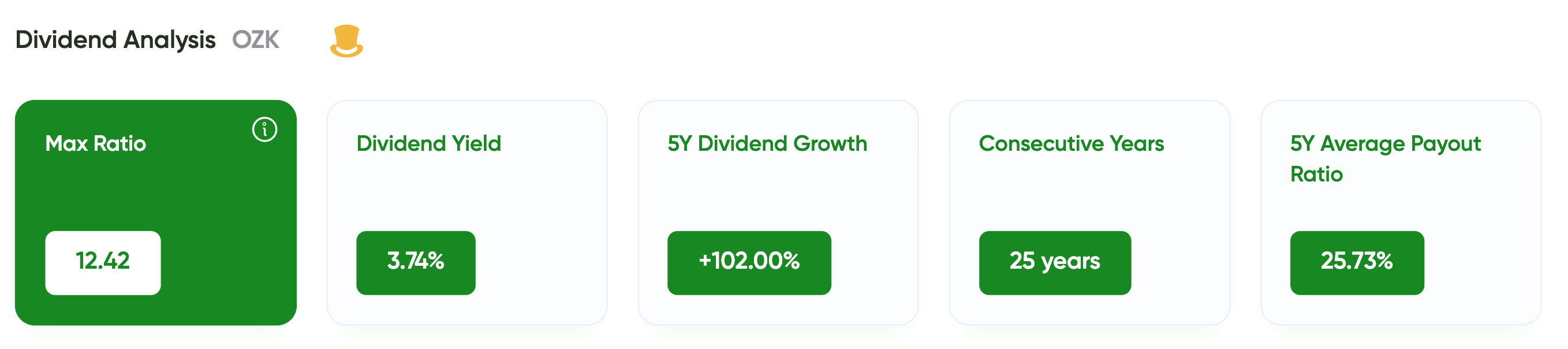

Let’s Look at Bank OZK (OZK)

Open the MaxDividends App → Company Analytics → place Financial Score next to MaxRatio. That’s where the role becomes obvious.

Here’s what OZK shows:

MaxRatio: 12.42

Dividend Yield: 3.74%

5Y Dividend Growth: +102% (cumulative)

Consecutive Dividend Years: 25 years

5Y Average Payout Ratio: 25.73%

With a MaxRatio above 12, OZK lands clearly in the Income Eagle category.

What that means in practice:

you’re getting a solid yield today (not extreme, but meaningful)

dividend growth has been very strong in recent years

the payout ratio is low — giving the dividend a real safety buffer

the company has a long dividend track record that supports “policy consistency”

Bank OZK works best as an income engine with growth on top — a position built to generate cash flow today, while still pushing that cash flow higher over time.

💵 Is the Stock Undervalued Today?

Cheaper than competitors?

🟢 Yes — Undervalued vs peers (per the MaxDividends App).

Quick note on what this measure actually means: the app compares OZK against 10+ banks in the same sector and looks at how strong its earnings per share are versus that peer group. Stronger EPS relative to peers typically signals you’re paying less for more profitability.

Cheaper than its own history?

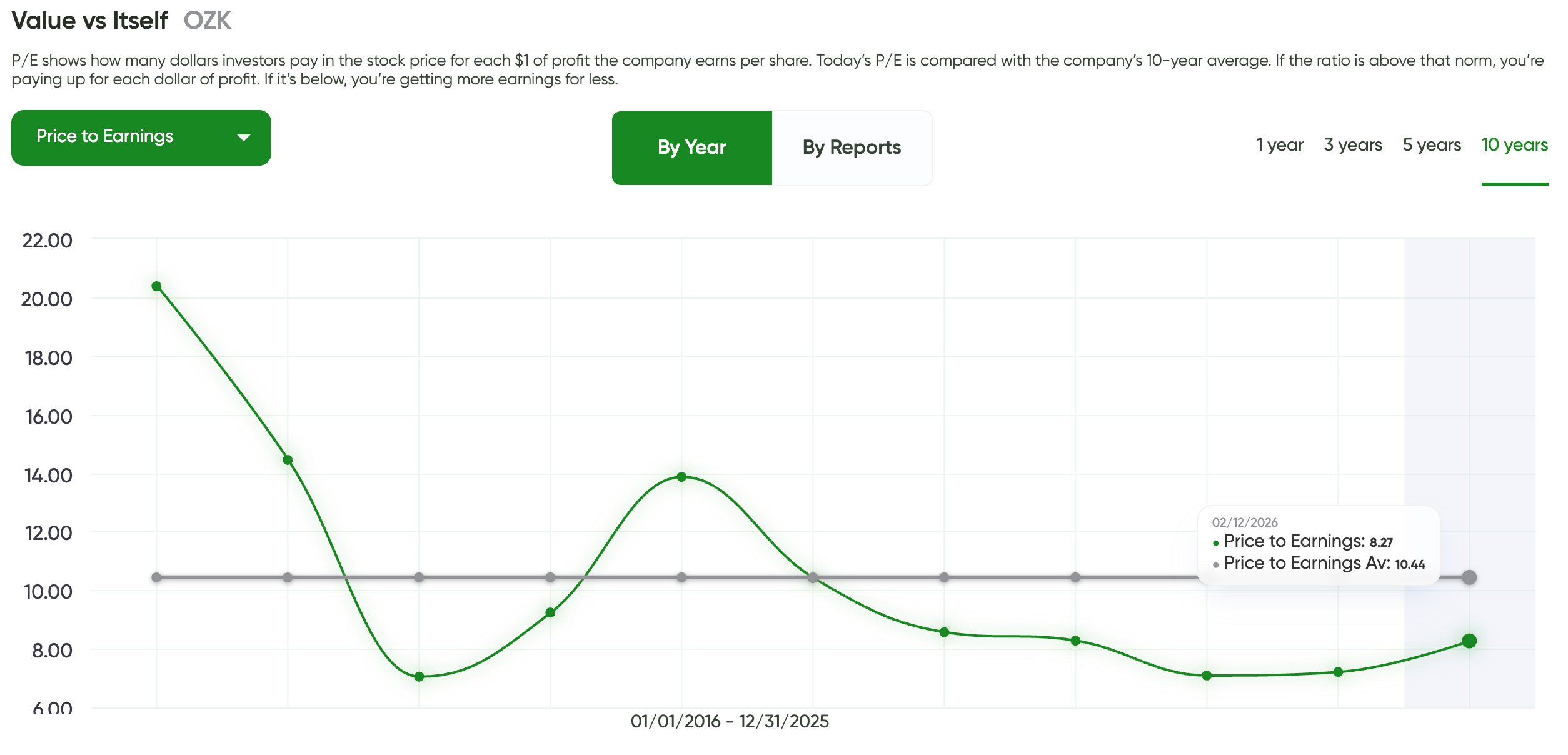

🟢 Yes — meaningfully cheaper than its 10-year norm.

Today’s P/E: 8.27

10-year average P/E: 10.44

That can happen for two reasons:

the market is underestimating durability (opportunity), or

the market is correctly pricing in cycle risk (warning)

Either way, the stock is priced like a more cyclical story than its long-term average suggests.

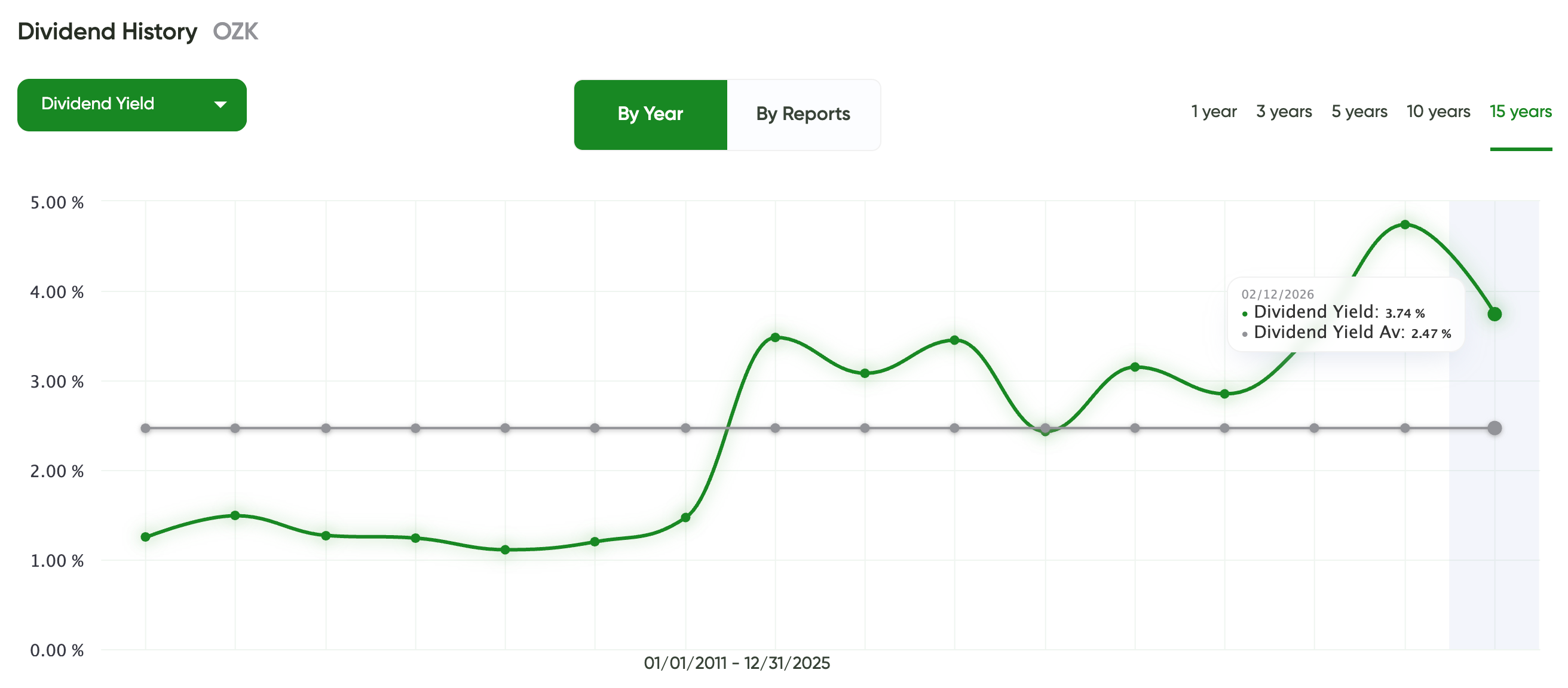

Better Yield Than Usual?

🟢 Yes — yield is above its historical average.

Dividend yield today: 3.74%

10-year average yield: 2.47%

A yield above the long-term norm usually shows up when:

the price is depressed, and/or

the dividend has been raised faster than the stock has rerated

We’re getting paid more than usual to own OZK today — which is exactly what income investors want as long as the dividend is structurally safe (and our payout metrics so far support that).

Analyst Consensus

Neutral — analysts see upside, but conviction is mixed.

On the Street, Bank OZK (OZK) is not a “unanimous buy” right now — it’s a split decision, which usually means the market is still debating the same thing we care about most: how the credit cycle plays out from here.

MarketBeat (11 analysts): consensus Hold, average 12‑month price target $56.78 (targets range $50–$67).

StockAnalysis (9–10 analysts depending on page): consensus Buy, average price target $53.67 (targets range $40–$62).

With OZK around $49.25 (as of Feb 12, 2026), those averages imply roughly ~9% to ~15% upside — but the wide target spread is the real signal: uncertainty is still elevated.

Is This One for Me?

Here’s how Bank OZK (OZK) stacks up under the MaxDividends lens:

How This Company Makes Money?

Do I clearly understand how OZK earns its money — and does the business actually make sense?

🟢 Yes.

OZK is a spread-driven bank: it gathers deposits, makes loans, and earns net interest income on the difference. That model is simple and understandable — but it’s also cycle-sensitive, because bank earnings ultimately depend on credit losses + funding costs + capital discipline (not consumer demand).

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience a long‑term dividend strategy needs?

🟢 Yes — with one condition.

OZK has shown real dividend consistency over a long period, and it scores Financial Score = 90 (“Very safe”) in the MaxDividends App — strong proof of fundamental quality.

The condition: as a bank (with meaningful real-estate / credit-cycle exposure), it’s not “set-and-forget.” Long-term ownership works best when you’re willing to monitor credit metrics and accept cyclicality.

Is the Stock Undervalued Today? 💵

🟢 Mostly favorable:

Vs peers: Undervalued (per MaxDividends App)

Vs its own history: Today’s P/E 8.27 vs 10-year average 10.44 (cheaper than normal)

Yield vs history: 3.74% today vs 10-year average 2.47% (you’re paid more than usual)

This is not a “no-risk bargain.” It’s a classic setup where the market prices in caution — and your job is to confirm the dividend is backed by structure (coverage + balance sheet), not vibes.

Does It Fit Your Plan?

Not every dividend stock has the same job. With:

MaxRatio: 12.42

Dividend yield: 3.74%

5Y dividend growth: +102% (cumulative)

5Y average payout ratio: 25.73%

Consecutive dividend years: 25

OZK lands clearly as an Income Eagle — an income-first holding that can still deliver meaningful dividend growth. What that means in practice:

you’re getting real income today, not a “tiny yield” placeholder

dividend growth has been strong, not symbolic

the payout ratio is low, which creates a buffer for rough patches

Best fit if your plan includes:

building a cash-flow engine inside a diversified dividend portfolio

buying quality banks when they’re priced with skepticism

being “paid to wait” while the cycle normalizes

Less ideal if you:

want a dividend stock you never have to monitor

can’t tolerate credit-cycle headlines and volatility

Final Take

Max’s Comment:

For me personally, this is one of the companies I like and invest in when conditions are favorable. As of today, my position is already established — it makes up about 3% of my portfolio, with an average purchase price of $41 per share.

It’s one of those businesses where I was able to lock in a strong dividend yield and build a solid margin of safety from the start by applying the best practices of the MaxDividends Income System framework through the app.

Bank OZK is a financially strong, dividend-disciplined bank that screens as undervalued and fits the portfolio as an Income Eagle: meaningful yield today, strong recent dividend growth, and conservative payout discipline.

But classify it correctly: this is cycle-aware income, not a utility-style sleep-well holding.

Used properly, OZK is a paid-to-wait dividend bank — where the edge comes from buying quality while the market is still cautious, and letting dividend compounding do the work.

***

The same simple formula works for any stock. No hype, no noise — just clear steps that let you see whether a company truly fits your plan.

And the best part? This isn’t theory. It’s all already built into the MaxDividends app: the Financial Score, the MaxRatio, the Top Dividend Eagles list, and even my own personal shortlist. Everything in one place, ready whenever you are.

MaxDividends is a treasure chest for dividend investors of any size and focus. Whether you’re after growth, balance, or pure income, you’ll find the tools and the community to back you up.

This series of case studies is here to show you just how simple — and powerful — dividend investing can be. One stock at a time, you’ll see the clarity, the confidence, and the peace of mind that comes from building your own growing stream of passive income.

Everything you’ve just read about — the dividend intelligence, the quality filters, the structured selection process, the portfolio tracking, the income optimization — is fully integrated inside the MaxDividends App.

The App brings together the strategy, the screening logic, the risk controls, the Dividend Eagles lists, and the Income Assistant into one structured environment. It’s where analysis turns into decisions, and decisions turn into measurable income.

Everything works together in one place, designed to make disciplined dividend investing clear, manageable, and repeatable over time.

If you want access to the full system — it begins inside the platform.

🔓 Request Free Early Access to the MaxDividends App 🔓

Unlock instant 🎁 access to the MaxDividends Income System & App, featuring our top undervalued dividend picks and the most promising dividend ideas for 2026.

With respect for your well-being,

Max