Lockheed Martin Corporation (LMT) - Safe Income… or a Hidden Risk?

A step-by-step company analysis that teaches you how to apply the MaxDividends strategy in real life.

MaxDividends Mission: Helping people build growing passive income, retire early, and live off dividends.

This series is part of the MaxDividends Academy — where we teach our proven secret Five-Pillar Formula in practice. Each lesson breaks down a real company, showing how to spot lasting dividend payers and avoid traps, step by step.

🔓 Request Free Early Access to the MaxDividends App

Learn Dividend Investing One Stock at a Time

🎓 MaxDividends Academy Case Study: Lockheed Martin Corporation (LMT)

Hey — Max here 💪

Before we dive in, let me say a few words.

What you’re about to read is the kind of research we typically reserve for our Premium work — high‑conviction, step‑by‑step analysis built for dividend investors who prioritize staying power over headlines. The work below is built for finding dividend payers that can stay reliable through multiple market regimes, not just look attractive in a calm quarter.

The aim is to identify businesses that can keep distributing cash when conditions tighten, avoid the “yield first, questions later” mistakes, and steadily turn earnings power into income you can actually plan around.

That requires a repeatable method. Cycle‑aware investing isn’t about guessing next month’s CPI print or trying to time the next rate cut. It’s about owning companies whose economics and capital allocation hold up when the environment changes — when inflation flares, financing costs jump, growth slows, or leadership rotates from one sector to another.

You’re getting a full look at that framework here. Going forward, we’ll highlight additional dividend opportunities, including names that don’t screen as obvious income plays today but have the ingredients to become durable dividend growers over time.

The advantage is rarely “secret information.” It’s doing the unglamorous work early, before a narrative becomes consensus, and pairing that research with a plan. Instead of buying a stock only after everyone agrees it’s safe, you define what you need from the position — income level, downside tolerance, and long‑run dividend growth — and then decide whether the current setup offers a fair trade.

A lot of investors define “essential” as whatever people buy every week: electricity, groceries, prescriptions. But in the real economy, essentials also include things you hope you never need — deterrence, readiness, secure systems, and the ability to respond when the world gets unstable.

That’s not a quarterly trend. It’s a permanent line item, shaped by geopolitics and multi‑year procurement decisions. For dividend investors, that makes the defense industry a unique hunting ground, and Lockheed Martin (LMT) one of the clearest case studies.

Lockheed Martin sits at the intersection of aerospace, defense technology, and long‑duration government contracting. The company is tied to programs that are expensive to replicate and politically difficult to unwind once deployed. LMT is not a consumer brand and it doesn’t rely on viral growth stories. It wins by engineering, integration, manufacturing execution, and the ability to deliver mission‑critical platforms on schedule with acceptable performance and cost.

That’s also why the business can look deceptively “steady” until something goes wrong: contract structures vary, development risk can surprise, supply chains can bite, and a single program issue can dominate headlines and near‑term results.

Still, the underlying model has traits that matter for income investors. A large portion of value in defense isn’t just the initial sale — it’s what happens after fielding: sustainment, modernization, training, software, parts, and service work that persists for years. That installed base effect can soften the blow when new awards slow or when procurement timing shifts.

And because the customer is primarily the U.S. government and close allies, demand isn’t driven by consumer confidence; it’s driven by strategic priorities, budgets, and threat environments that tend to play out over long horizons.

The nuance is important. Defense is not “non‑cyclical” in the way utilities can be. It’s cyclical in a different way: funding can be reallocated, programs can be stretched, contracts can be renegotiated, and political attention can turn quickly if execution stumbles. For a dividend investor, the central question is not whether LMT can generate strong years — it has proven that.

The real question is whether the company’s cash generation is resilient enough, and its financial policy conservative enough, to protect the dividend when the cycle turns against it through delays, cost pressure, or a less favorable mix of work.

Lockheed has a long record of treating shareholder returns as a priority, and the dividend is a major part of that identity. But reputation isn’t a substitute for math. A dividend is only as durable as the cash that funds it, and the discipline that prevents management from overreaching when times are good.

What matters is whether the payout is supported by repeatable free cash flow after the business is properly maintained — not temporarily boosted by working‑capital timing, not protected by adding leverage, and not masked by buybacks that are out of sync with underlying fundamentals.

The real question is:

Does Lockheed Martin fit your plan right now — at today’s valuation, yield, and realistic dividend growth outlook — or is it better treated as a watchlist name until the setup becomes more attractive?

In this Deep Dive, Lockheed Martin goes through the MaxDividends Five‑Pillar Formula — the same grounded checklist we use to evaluate whether a dividend payer can keep compounding income through recessions, inflation waves, and market stress, without relying on perfect conditions to make the payout work.

👉 Let’s break it down — step by step.

How This Company Makes Money?

Do I clearly understand how Lockheed Martin Corporation (LMT) earns its money — and does the business make sense?

Lockheed Martin designs and builds advanced defense and aerospace systems, but the real compounding machine is the combination of a massive installed base already fielded with the U.S. and allied militaries and a long-tail sustainment and modernization ecosystem that supports, repairs, upgrades, and supplies parts over decades.

Cash flow is driven by procurement demand across budget and threat cycles plus the high‑value aftermarket-like stream that comes from keeping platforms mission-ready — not by consumer branding, advertising spend, or rapid product-fashion cycles.

1️⃣ Platform Leadership + Installed Base

LMT’s edge is that each delivery expands the installed base. Over time, that installed base becomes a durable economic asset: systems need maintenance, spares, software updates, upgrades, training, and periodic modernization. In good years, production volume lifts results. In softer years, the installed base helps cushion profitability because fleets still need to operate.

2️⃣ Sustainment Ecosystem

Lockheed’s sustainment footprint is not just a revenue line — it’s a competitive moat. It provides logistics, depot and field support, parts availability, engineering changes, upgrades, and deeply embedded customer relationships that are hard for competitors to replicate at scale. For dividend investors, this matters because it keeps LMT close to end demand, increases capture of long-tail support dollars, and helps protect program position even when buyers get budget‑sensitive. It also improves resilience: when procurement slows, sustainment work and spares logistics remain active because downtime is unacceptable for customers.

3️⃣ Parts, Spares, and Modernization

In defense, the “razor-and-blades” dynamic is real. Sustainment, spares, and modernization often carry steadier demand than new production, because keeping high-end platforms ready is non‑optional. This is one reason Lockheed can be a dividend investor’s cyclical: you’re not underwriting only the next procurement cycle — you’re underwriting a long stream of repair, replacement, upgrade, and refresh activity tied to the installed base. Higher sustainment penetration also tends to increase customer stickiness: once logistics systems, technical data, and support workflows are embedded, switching costs rise.

4️⃣ Execution Discipline + Capital Allocation

Lockheed doesn’t compound like a high-growth tech firm. Its long‑term compounding mechanism is industrial: program execution, risk control, supply-chain discipline, cost productivity, and thoughtful capacity decisions — while continuing to invest in engineering reliability and customer support.

The key strength is that Lockheed operates in a foundational pillar of the modern world: deterrence, readiness, and allied security. Those priorities can shift — but they don’t disappear. Systems still break, fleets still age, threats still evolve, and missions still need to be supported. That doesn’t make LMT recession‑proof, but it does make the business model easier to underwrite than many high-yield setups that depend on permanently favorable conditions.

It’s not a black box. It’s an installed-base-and-sustainment ecosystem built to win through readiness, customer integration, and lifetime program economics — the kind of structure that can support a long dividend record when paired with conservative financial management.

👉 And yes — this business model is clear, resilient, and makes perfect sense.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience a long‑term dividend strategy needs?

Our approach is simple, but it works: we focus on businesses that can generate repeatable cash flow through an entire cycle and translate that cash into reliable, growing dividends. With a company like Lockheed Martin, the goal isn’t to pretend the business is “risk‑free” or immune to politics, budgets, and program execution.

It’s to own a defense prime with cycle-tested characteristics and the tools to endure rough patches: a large installed base that drives long-tail sustainment and upgrade demand, deep customer embedment that makes platforms hard to replace once fielded, and operating discipline that prioritizes free cash flow and program performance over chasing headline growth at any cost.

The MaxDividends Strategy Checklist – Simple Steps to Pick the Right Stocks

Step 1: Dividend History

Our filter: Companies with 15+ years of consistent dividend growth.

Lockheed Martin doesn’t just “qualify” on dividend consistency — it displays the kind of steady, stair‑step progression long‑term dividend investors look for, and it does it in a business where risks show up in different forms than a typical consumer company. LMT’s annual dividend per share climbed from roughly $3 in the early 2010s to about $13+ most recently.

That shape matters because it points to a payout supported by repeatable cash generation and a management culture that treats the dividend as a core commitment, not something to be adjusted opportunistically when conditions feel comfortable.

For a defense prime exposed to program execution risk, contract timing, shifting budget priorities, and occasional political scrutiny, that consistency is not automatic. It suggests Lockheed has been able to generate sufficient free cash flow across very different environments and manage the balance sheet conservatively enough to avoid reactive decisions when a program gets noisy or the headlines turn.

This is what a real aerospace-and-defense income compounder looks like in practice: not a gimmicky yield story, not a one‑time special dividend narrative — but a methodical pattern of annual raises that reflects long‑term capital allocation discipline.

✅ Step 1 passed — Lockheed Martin (LMT) behaves like a Dividend Eagle, with a durable record of dividend increases that holds up despite program and budget cycles and supports the case for LMT as a serious dividend-growth candidate.

Step 2: The Five-Pillar Secret Formula

1️⃣ Sales Growth – The Foundation of a Strong Business

On the 10‑year view, Lockheed Martin’s sales rose from roughly the mid‑$47B range in the mid‑2010s to about $75B most recently. The path isn’t perfectly smooth — and it shouldn’t be. LMT is tied to defense budgets, program timing, contract mix, and the cadence of deliveries and milestone funding. But the long‑term direction is clearly higher.

That pattern fits the reality of Lockheed’s business model. LMT doesn’t grow because of consumer “discovery” or marketing-driven demand. It grows when it secures and executes major programs, expands the installed base of fielded platforms, and captures more lifetime value through sustainment, upgrades, spares, and modernization work that extends across decades. Over time, that ecosystem can lift revenue even if individual years are influenced by procurement schedules and program-specific noise.

✅ Sales Growth Passed — Lockheed Martin’s higher long‑term revenue base supports the view of LMT as a durable defense platform with a credible foundation for dividend growth.

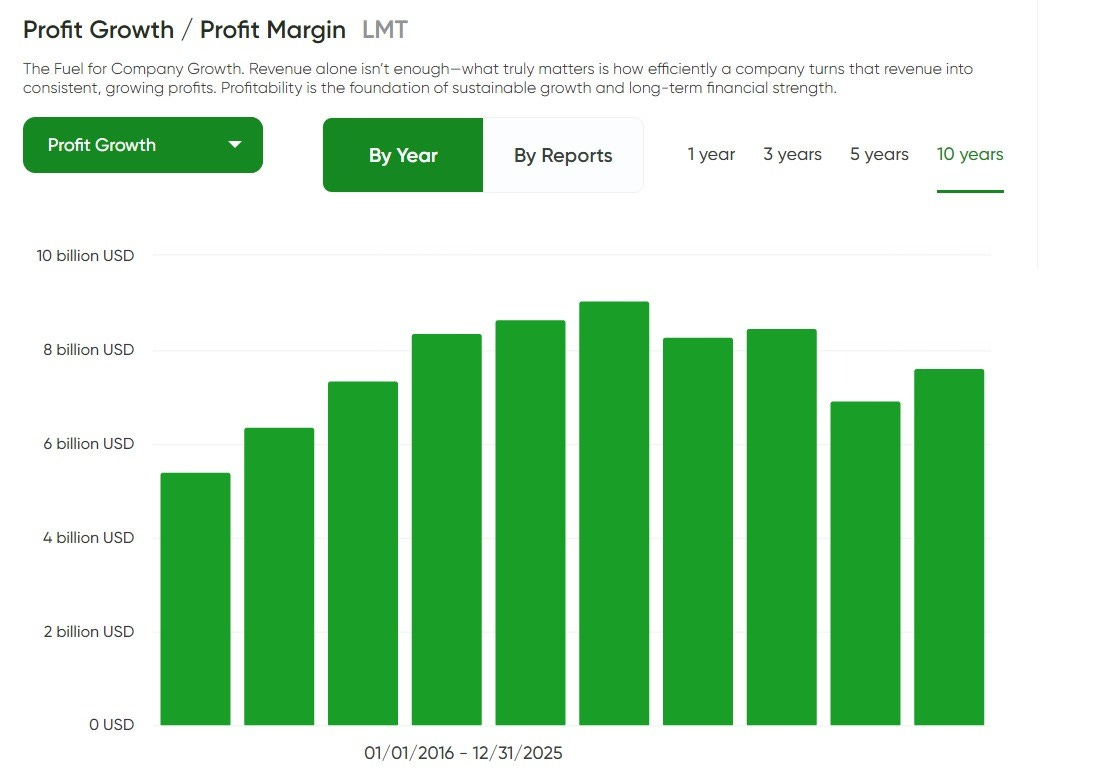

2️⃣ Profit Growth – The Fuel for Dividend Growth

Lockheed Martin’s profit trend reinforces the same message as the revenue line — but with an added layer of confidence: profitability has held up over time in a way that looks durable rather than dependent on a single “perfect” year. Over the last decade, profits build from roughly the mid‑$5B range to around the mid‑$7B range most recently.

The path isn’t a straight climb; there’s a clear rise into the late‑2010s, followed by a choppier stretch and then stabilization. For a defense prime, that matters. It suggests Lockheed isn’t simply benefiting from a temporary procurement surge, but operating from a profit base that can persist even as program timing and contract mix shift.

The “why” matters, because this isn’t a story about Lockheed suddenly finding a fashionable growth pocket. In aerospace and defense, the compounding mechanism is execution and installed‑base economics. When program performance is tight and contract risk is managed well, profitability can remain resilient even if reported sales growth is uneven.

As the installed base expands, sustainment, spares, and modernization activity tends to follow, helping support profit quality because readiness work is less optional than new awards. And when productivity efforts and cost discipline are applied consistently, small operational gains can translate into meaningful profit stability over time.

✅ Profit Growth Passed — Lockheed Martin’s durable profit base strengthens dividend reliability and supports the case for continued dividend growth while maintaining the flexibility needed to navigate program and budget cycles.

3️⃣ Net Income – True Measure of Strength

Lockheed Martin’s net income trend is a strong example of what dividend investors should look for: a generally solid earnings base across the decade, with enough variation to act as a real-world stress test without breaking the long-term dividend story. Over the 10‑year view, net income sits around the mid‑single‑digit billions for much of the period, reaching roughly the $6–$7 billion range at its stronger points, and easing back toward about $5 billion in the most recent years.

The profile includes a noticeable dip early in the window, a rebound into a higher earnings zone, and then a choppier stretch where results fluctuate rather than marching in a straight line.

That pattern is exactly why we focus on direction and durability rather than demanding a perfectly smooth line. Lockheed operates in a world of program cycles, contract timing, and execution risk, so earnings can move around even when the strategic demand backdrop is supportive.

What matters for dividend compounding is whether the business can maintain a healthy earnings base through those shifts and avoid permanent impairment when a year turns unfavorable. In Lockheed’s case, the answer appears to be yes: profitability remains firmly positive across the decade, and the company demonstrates the ability to recover after weaker periods rather than sliding into a lasting downtrend.

✅ Net Income Passed — Lockheed Martin shows a resilient underlying earnings profile over the decade, reinforcing that its dividend growth is supported by real operating staying power rather than a temporary tailwind.

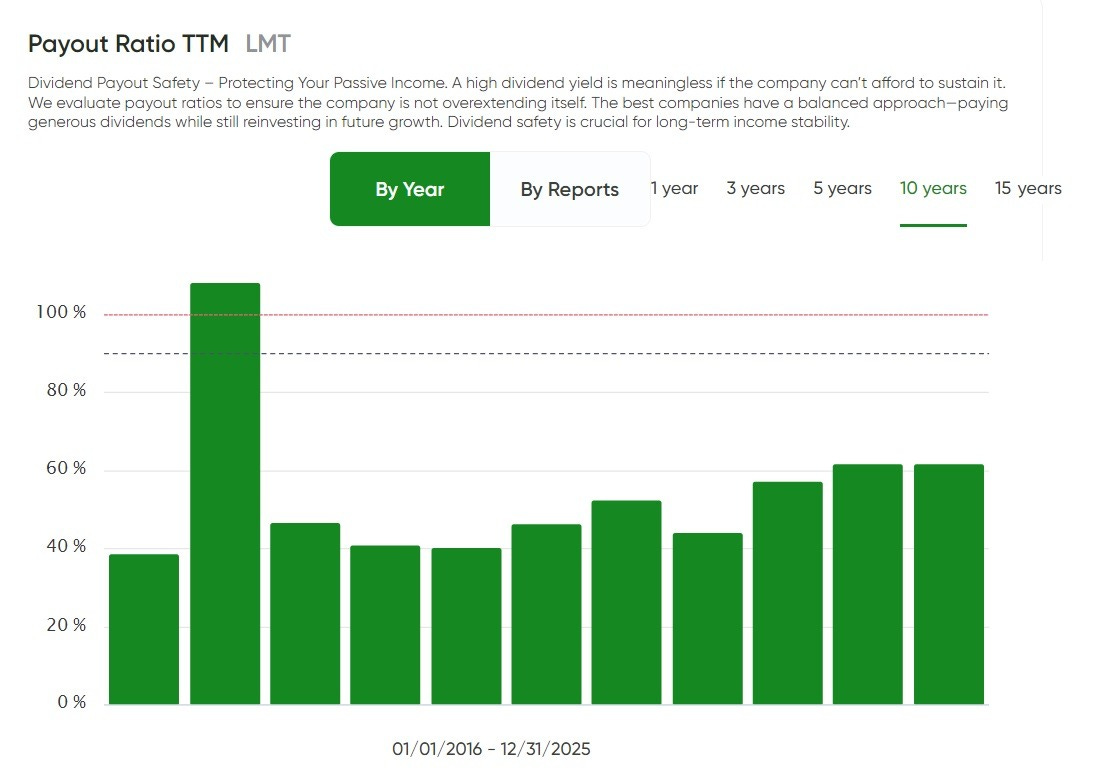

4️⃣ Dividend Payout Safety – Protecting Passive Income

For Lockheed Martin, the payout ratio story is a good example of why dividend investors should treat this metric as a signal that needs context, not as a simple “safe/unsafe” label. Over most of the period, LMT’s payout ratio sits in a fairly reasonable range for a mature defense contractor with a shareholder-return focus, often clustering in the ~40% to ~60% zone. Then you see the outlier: a one‑year jump to a little above 100%, before the payout ratio drops back down and resumes a more normal band afterward.

The reason matters, because this doesn’t automatically describe a dividend that’s structurally out of control. It’s what a payout ratio looks like when earnings take a temporary hit while management chooses to keep the dividend on its planned path.

In Lockheed’s case, the spike suggests that reported net income was unusually pressured in that period, so the dividend became large relative to the depressed earnings base. In plain terms, the ratio didn’t surge because the dividend suddenly turned reckless — it surged because the denominator weakened.

What dividend investors should focus on is what came next. The payout ratio normalizes back into a sustainable range, which implies earnings power recovered and coverage improved.

That’s the behavior you want to see in a business exposed to program timing and execution variability: a temporary distortion during an earnings hit, followed by a return to normal as the company re‑establishes its profit base while maintaining the dividend through the noise.

✅ Dividend Payout Safety Passed — despite a temporary distortion during an earnings dip, Lockheed Martin’s payout ratio has returned to a more sustainable range, supporting the view that the dividend is affordable under normal conditions and can keep compounding without forcing the balance sheet into a corner.

5️⃣ Debt Burden – Avoiding Financial Traps

Lockheed Martin does use debt, and that shouldn’t automatically scare dividend investors off. Aerospace and defense is capital- and R&D-intensive, with long program timelines and working-capital demands that can shift around deliveries and milestone billing.

The real question isn’t whether leverage exists, but whether it’s controlled and stable — or whether it’s trending in a way that eventually forces uncomfortable tradeoffs between investment, buybacks, and the dividend.

On the 10‑year debt ratio view, Lockheed’s leverage looks elevated but managed. The ratio moves within a fairly contained band for most of the period, generally sitting around the high‑0.8s to roughly ~1.0 early on, dipping to about ~0.78 in the middle years, and then settling back near the high‑0.8s more recently.

That’s what “managed leverage” tends to look like in a mature contractor: not debt‑free and not ultra‑conservative, but also not showing the kind of balance-sheet deterioration that typically precedes dividend stress.

⚠️ Debt burden — leverage is clearly on the high side, and that’s the main constraint dividend investors should keep in mind. The encouraging part is that the ratio has stayed broadly stable rather than compounding higher year after year, which reduces the odds of near-term dividend pressure.

But if leverage starts trending upward again from here, it would be a meaningful negative: it would signal shrinking financial flexibility and increase the risk that future capital allocation choices begin to compete directly with dividend growth.

Bottom Line: The Company Financial Condition?

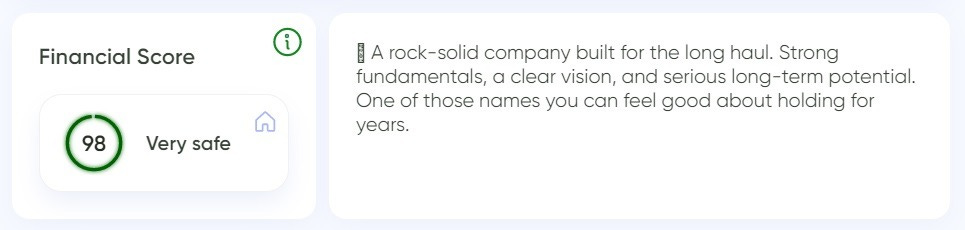

Financial Score 90+ ✅

For Lockheed Martin (LMT), the Financial Score comes in at 98 (“Very safe”). That clears our 90+ threshold with room to spare and points to a financial profile built for resilience — exactly what dividend investors want when the plan is to hold through multiple environments, not just the next quarter.

In practical terms, a score in this range supports the idea that Lockheed has the balance-sheet strength and cash-generation capacity to navigate program timing, execution noise, and shifting defense-budget priorities, keep investing in core capabilities and long-tail support infrastructure, and still protect the dividend strategy without being forced into reactive capital allocation decisions at the wrong time.

MaxDividends Five-Pillar Secret Formula. Step 2 - ✅

Lockheed Martin (LMT) comes out of our Five‑Pillar review looking like the type of dividend stock you can realistically own through a full cycle — not just a name that works when conditions are calm and headlines are friendly.

The dividend record is the first clue. Lockheed’s payout history shows the stair‑step pattern long‑term income investors look for, reflecting a dividend that’s treated as a priority and raised steadily over time. The business fundamentals support that interpretation.

Over a decade-long view, Lockheed operates from a larger revenue base than it did in the mid‑2010s, and its earnings profile has remained resilient as well, even as results move around based on program timing and contract dynamics rather than consumer-driven demand.

The “messy” part in the beginning of the period matters, because it isn’t random. Lockheed’s financials can be influenced by execution on complex programs, shifts in mix between development and production work, delivery cadence, and periodic budget or procurement timing changes. The dividend investor takeaway isn’t that LMT is immune to disruptions — it’s that the company has shown an ability to take volatility in stride without breaking the underlying earnings engine that supports shareholder returns.

That context also explains why payout metrics can briefly look uncomfortable. When earnings are pressured in a given year, the payout ratio can spike even if the dividend itself remains stable and policy-driven. What matters is whether that distortion is temporary and whether coverage improves as earnings normalize.

In Lockheed’s case, the more typical payout levels outside the spike suggest the dividend is still anchored to a sustainable earnings base rather than being propped up indefinitely.

Leverage is part of the picture as well, and this is where dividend investors should stay alert. Lockheed carries a relatively high debt load, and while the trend has been broadly managed rather than steadily deteriorating, further leverage creep from here would be a real negative.

Higher debt would tighten financial flexibility and increase the chance that future capital allocation decisions begin to compete directly with dividend growth, especially during periods of program noise.

Taken together, Lockheed doesn’t just clear the checklist — it clears it with authority. A Financial Score of 98 places it firmly in our “very safe” tier and supports the view that LMT’s dividend profile is backed by durable operating capacity, with real-world variability serving as proof of resilience rather than a permanent weakness

✅ Passed: Lockheed Martin (LMT) — Proven Dividend Eagle.

Does It Fit My Plan?

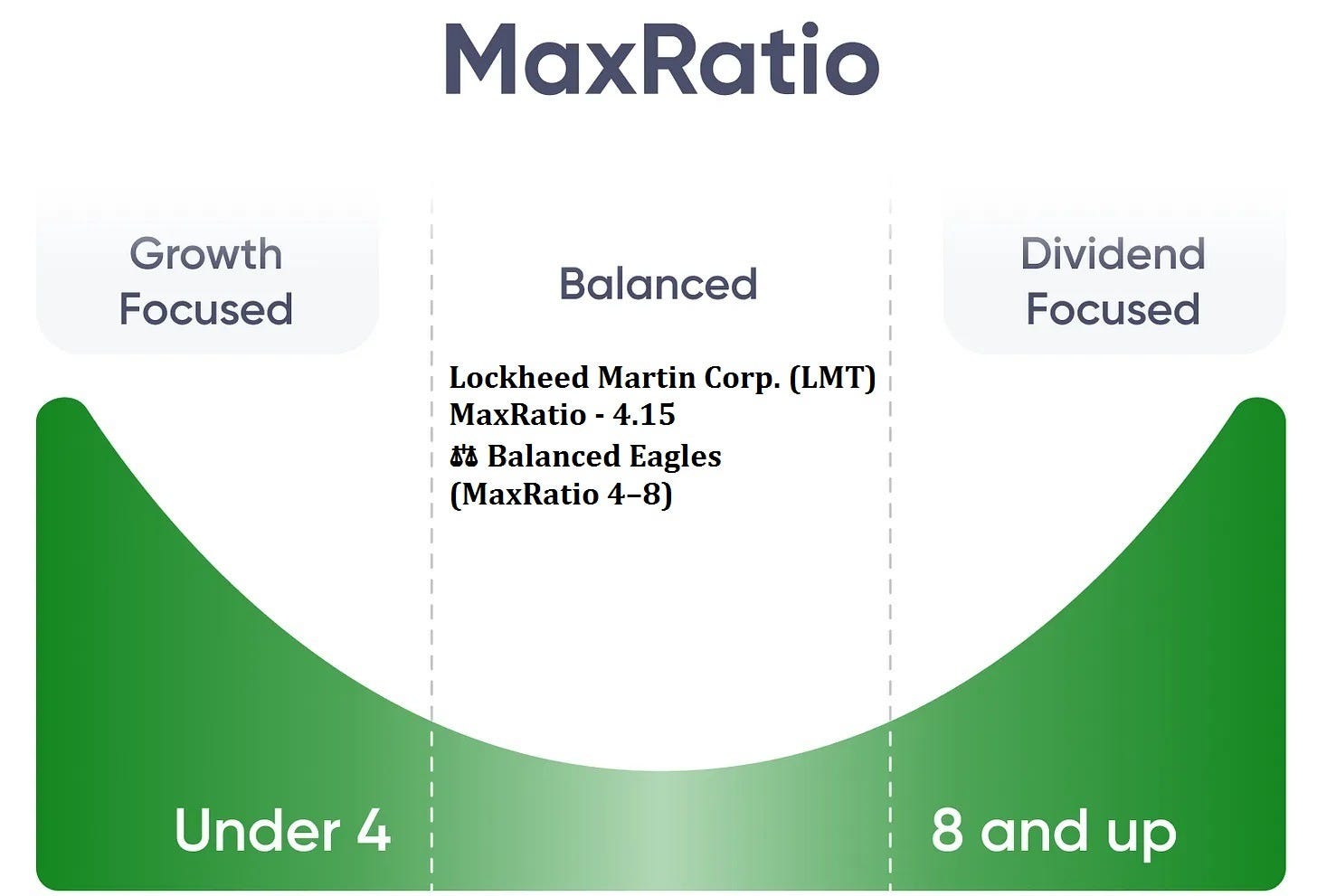

Finding the Right Role for Every Dividend Stock – MaxRatio

Dividend stocks aren’t one-size-fits-all, and treating them that way is a common route to disappointment. The label “dividend stock” covers very different kinds of holdings: some are built to be held for decades as quiet compounders, others earn a core slot because they combine income with durable growth, and a smaller group is mainly about generating the most cash right now.

That’s exactly what MaxRatio is for. It’s a practical way to match a dividend stock to its most logical job in a portfolio using three inputs that matter in real life: today’s dividend yield, the pace of dividend growth, and the company’s overall financial strength. When you evaluate those signals together, it becomes clearer whether a stock belongs in a growth-leaning bucket, a balanced core allocation, or an income-first sleeve.

🚀 Growth Eagles (MaxRatio under 4) — are usually owned for long-run compounding. The starting yield tends to be modest, but business quality and reinvestment capacity can drive faster earnings and dividend growth over time.

⚖️ Balanced Eagles (MaxRatio 4–8) — often land in the “sweet spot” for many dividend investors. You get a respectable yield today, while dividend growth is typically strong enough to keep lifting your income stream and support price appreciation through a full cycle.

💵 Income Eagles (MaxRatio 8+) — are designed primarily for near-term cash flow. They often offer higher yields upfront, but dividend growth can be slower, making them a better fit for investors who prioritize current income over maximizing long-term total return.

MaxRatio isn’t meant to label Lockheed Martin (LMT) as “good” or “bad.” It’s meant to answer the more practical question: what role should this stock play in a dividend portfolio? With Lockheed, you’re generally looking at a business where dividend reliability is supported by long-cycle defense programs and a large sustainment footprint, not by an attention-grabbing yield. In most setups, it fits best as a core, plan-friendly holding for investors who want income that can grow steadily over time, with the main caveat being that higher debt and program execution noise are risks worth monitoring rather than ignoring.

Let’s Take Lockheed Martin Corporation (LMT)

Inside the MaxDividends app, you can open Company Analytics and, in seconds, pull the two numbers that matter most for quick dividend positioning: the Financial Score and MaxRatio. No spreadsheets, no jumping between tabs — just a clean read on quality and portfolio role.

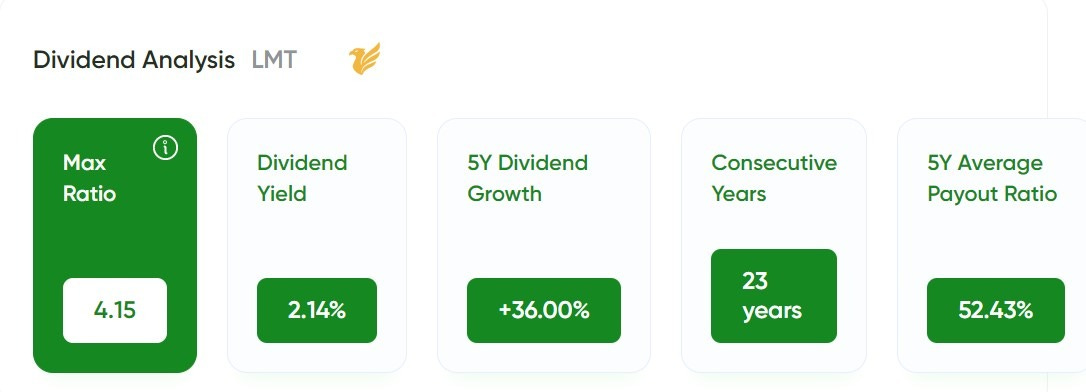

For Lockheed Martin (LMT), the MaxRatio snapshot lands in the balanced zone of the framework. LMT shows a MaxRatio of 4.15, which places it in the Balanced Eagles (MaxRatio 4–8) category. In plain English, this is a dividend profile where you’re not choosing between yield and growth — you’re getting a workable mix of both, assuming the business continues to execute.

That positioning fits Lockheed’s reality. With a dividend yield of roughly 2.14%, the stock offers meaningful income today without leaning into “high yield” territory. What supports the case is that dividend growth has still been respectable, with +36.00% growth over the last five years, backed by a long record of shareholder commitment reflected in 23 consecutive years of dividend payments.

LMT’s 5‑year average payout ratio of 52.43% reads like a mature, shareholder-return-oriented policy with some buffer, but not unlimited room. The bigger point for dividend investors is that Lockheed’s earnings can be influenced by program timing and execution, and the balance sheet carries a relatively high debt load, which means sustained leverage expansion would be a genuine negative for future flexibility. The takeaway is that LMT looks less like an income-maximizer designed to throw off the most cash immediately, and more like a core, balanced dividend holding where income can keep rising at a steady pace — as long as execution remains solid and leverage stays controlled.

For investors building a dividend portfolio with a long runway, Lockheed’s role is relatively clear. It’s not a pure high-yield anchor, and it’s not a low-yield hyper-growth dividend story either. It’s positioned as a balanced core: a solid starting yield, healthy recent dividend growth, and a payout profile that looks sustainable under normal conditions — giving the company room to keep raising the dividend over time without turning the balance sheet into the limiting factor.

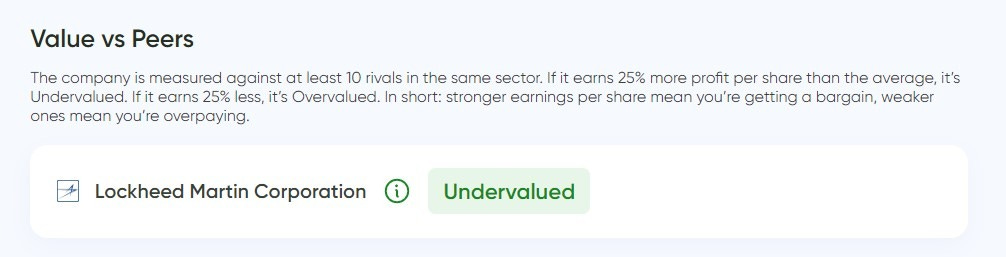

💵 Is the Stock Undervalued Today?

Cheaper than competitors?

🟢 According to the MaxDividends App, Lockheed Martin (LMT) currently screens as Undervalued versus its peer group.

“Undervalued” doesn’t automatically mean Lockheed is a can’t-miss bargain — and it doesn’t mean the stock has to re-rate upward immediately. It means that, relative to a peer set of comparable aerospace and defense contractors, the market is assigning LMT a cheaper-than-average valuation for its current profit profile.

Cheaper than its own history?

⚠️ More expensive vs. its own 10-year average.

On a “value vs. itself” basis, Lockheed Martin (LMT) doesn’t screen as cheap versus its own history — and in this case the comparison is usable. The current P/E is about 30.03, while the 10‑year average shown is about 21.53. The market is valuing Lockheed at a noticeably higher multiple than it has averaged over the last decade.

That doesn’t automatically mean LMT is a bad dividend buy, but it does change the setup. When a stock is priced above its typical historical multiple, your forward returns lean more heavily on fundamentals continuing to deliver — steady execution, dependable cash conversion, and ongoing dividend growth — rather than getting an extra boost from valuation expansion.

The practical takeaway for dividend investors is to treat the “undervalued vs peers” signal and the “premium vs its own history” signal together rather than in isolation. LMT may look inexpensive relative to other defense names today, but it’s still trading above its own long-run average multiple, which suggests the margin of safety is more about business quality and dividend durability than about a clearly depressed valuation versus its past.

Better Yield Than Usual?

⚠️ Yield below its 10-year average.

Right now, Lockheed Martin (LMT) is yielding about 2.14%, while its long-term average yield over the 15-year view sits near 2.89%. That spread tells you the starting income today is below what investors have typically received over this period, which usually happens when the share price is firm relative to the dividend and the market is not offering an especially generous entry yield.

In plain English, LMT is offering less income than usual versus its own history. That doesn’t make it a weak dividend stock — Lockheed’s appeal is that it combines a respectable yield with consistent dividend growth and long-cycle cash-generation characteristics — but it does mean you’re not buying at a “historically high yield” point.

Analyst Consensus

⚠️ Analysts don’t see meaningful short-term upside for Lockheed Martin Corporation (LMT).

The average 12‑month price target for Lockheed Martin is about $657.58, implying roughly +1.85% upside from current levels. The target range is still meaningful — from around $517.00 on the low end to about $740.00 on the high end. Overall consensus leans Neutral.

In plain English, analysts see LMT as having only limited upside over the next year, with outcomes still wide enough to reflect real uncertainty — which is typical for a defense prime where program execution, contract timing, and sentiment around budgets can swing expectations. For dividend investors, that’s a useful framing: the case for owning Lockheed isn’t about a quick re-rating or a near-term “pop,” especially with the stock yielding below its long-term average.

Is This One for Me?

Here’s how Lockheed Martin stacks up under the MaxDividends lens:

How This Company Makes Money?

Do I clearly understand how Lockheed Martin (LMT) earns its money — and does the business make sense to me?

🟢 Yes: a scale-driven defense-and-aerospace ecosystem built on a massive installed base of mission-critical platforms, long-cycle government programs, and recurring sustainment and modernization demand. Lockheed Martin makes money primarily by delivering major systems to the U.S. and allied customers, then monetizing the decades-long lifecycle that follows through sustainment, spares, upgrades, training, and ongoing support tied to keeping fleets and systems mission-ready.

Is This a Good Stock to Buy Long Term?

Has the company shown the kind of consistency and resilience I want to see?

🟢 Yes: Lockheed Martin has demonstrated the kind of durability dividend investors look for, including through real-world operating and program volatility. The company has built a long record of dividend increases, and its dividend history shows the steady, upward “stair-step” profile that typically signals a payout guided by policy and discipline rather than a temporary good stretch.

What makes Lockheed’s record more convincing is that this isn’t a business where everything moves in a smooth line. Results can be influenced by program execution, contract timing, and mix shifts, and those factors can pressure earnings in specific years even when the long-term demand backdrop remains supportive. Yet through those uneven patches, Lockheed has maintained its dividend posture and then improved coverage as profitability normalized. That sequence matters because it shows resilience in practice — not just in theory — and it supports the case that dividend growth is being funded by a business with staying power, not a one-off tailwind.

Is the Stock Undervalued Today? 💵

⚠️ It looks undervalued versus peers, but the “value vs. itself” picture is stretched, and the current yield is still below its long-term average. In the MaxDividends app, Lockheed Martin screens as Undervalued relative to its peer group, which implies the market is offering a relative discount versus comparable aerospace and defense names based on its current profit profile.

At the same time, LMT’s “value vs. itself” comparison points the other way. The current P/E is around 30.03 versus a 10‑year average near 21.53, which suggests the stock is trading at a premium to its own historical multiple even if it looks cheaper than peers today. For dividend investors, that’s a reminder that “undervalued” can be a relative statement: the peer group may be priced richly, or Lockheed’s current earnings may be viewed as unusually durable, but you’re still not buying at a clearly depressed valuation versus LMT’s own history.

The yield picture is more straightforward and also argues against calling this a “historically generous” income entry point. Lockheed’s dividend yield is about 2.14% today versus a long-term average near 2.89%, meaning the starting income is lower than what investors have typically received over the last 15 years. Put differently, you’re getting a solid yield — just not a high-yield setup relative to its own past.

Taken together, Lockheed doesn’t read like a classic deep-value dividend entry right now. It looks more like a high-quality dividend payer that’s discounted relative to peers, but still priced above its own long-run average multiple, with a yield that’s below normal for LMT historically. For dividend investors, that can still be workable if the goal is dependable income growth from a durable franchise — but it’s not the kind of setup where the valuation and yield do all the heavy lifting for you.

Does It Fit Your Plan?

Dividend investing works best when each position has a job. If you treat every “dividend stock” as the same product, you end up with a portfolio that looks diversified on paper but behaves like a collection of mismatched bets. In my framework, dividend names usually fall into two buckets: anchors that deliver meaningful income from day one, and builders that start smaller but can grow into serious income producers as the dividend compounds.

Lockheed Martin (LMT) sits closer to the middle of that spectrum, but it leans more like a core builder than a true income anchor. The MaxRatio reading of 4.15 places it in the Balanced Eagle category, which lines up with what you see in the yield: the current payout is meaningful, but it’s not the kind of high-coupon dividend designed to maximize cash flow immediately. What you’re really buying with LMT is a long record of dividend increases paired with a business model that can support continued, steady payout growth when execution stays on track.

The underlying logic is straightforward. Lockheed operates on long-cycle programs and will always carry some “lumpiness” from contract timing and program execution, but it isn’t a one-time equipment delivery story. A large installed base of fielded platforms creates ongoing sustainment, spares, and modernization demand, and deep customer embedment makes those relationships durable and difficult to displace. That ecosystem is why the company can work through uneven years, re-establish cash-flow normalcy, and keep the dividend moving higher even when the operating backdrop gets noisy.

So LMT tends to fit best for dividend investors who want a plan-friendly core holding: people who value a solid starting yield, can tolerate program-driven variability, and want a high-quality defense franchise where dividend growth and long-run compounding do most of the work.

Final Take

Lockheed Martin has earned its reputation in a “real-world essential” way: it builds and integrates mission-critical defense and aerospace systems, and it supports them for decades through sustainment, spares, and modernization work that’s hard to replicate at scale. For dividend investors, the appeal isn’t a flashy yield story. It’s the combination of a long-running dividend commitment and a business that stays relevant as long as readiness, deterrence, and allied security remain structural priorities. The dividend history reflects that culture — steady, policy-driven increases rather than opportunistic payouts that vanish when conditions get uncomfortable.

The nuance is the entry point. On a peer-relative basis, the MaxDividends App frames Lockheed as undervalued versus its comparison set, which suggests you’re not paying a premium relative to similar defense names. On a “versus itself” basis, though, the P/E comparison points the other way: with a current multiple around 30.03 versus a 10‑year average near 21.53, LMT is trading above its typical historical valuation even if it looks cheaper than peers today. Meanwhile, the yield is the cleanest timing signal: at roughly 2.14% today versus a long-term average near 2.89%, the starting income stream is solid, but it’s still below what investors have usually been able to lock in for this company.

Put together, Lockheed clears the quality bar as a Proven Dividend Eagle and can make sense as a long-duration core dividend holding for investors who want defense exposure with a shareholder-friendly policy. But the current setup looks more like a “quality at a fair price relative to peers” situation than a classic “high-yield, historically cheap” entry. If the price softens enough to lift the yield closer to its long-term range — or if the stock’s valuation versus its own history compresses — the risk/reward profile becomes materially more attractive for conservative dividend investors.

***

The same simple formula I just used for Lockheed Martin works for any stock. No hype, no noise — just clear steps that let you see whether a company truly fits your plan.

And the best part? This isn’t theory. It’s all already built into the MaxDividends app: the Financial Score, the MaxRatio, the Top Dividend Eagles list, and even my own personal shortlist. Everything in one place, ready whenever you are.

MaxDividends is a treasure chest for dividend investors of any size and focus. Whether you’re after growth, balance, or pure income, you’ll find the tools and the community to back you up.

This series of case studies is here to show you just how simple — and powerful — dividend investing can be. One stock at a time, you’ll see the clarity, the confidence, and the peace of mind that comes from building your own growing stream of passive income.

🔓 Request Free Early Access to the MaxDividends App 🔓

Unlock instant 🎁 access to the MaxDividends Income System & App, featuring our top undervalued dividend picks and the most promising dividend ideas for 2026.

With respect for your well-being,

Max